The digital transformation in Egypt derives, its importance from the Sustainable Development Goals (Egypt Vision 2030) to reduce borrowing in addition to reducing public debt and the sustainability of financial inclusion, and this is achieved through financial discipline, which is one of the most prominent topics that have received wide attention in many developed countries, perhaps the accounting requirements to achieve institutional reform contributes greatly to financial discipline, especially with financial inclusion, especially when preparing the public budget in order to measure the ability of public expenditure to achieve sustainable development indicators, from the ability to manage financial expenditure, and revenues accurately and in a way that responds to financial goals after reviewing the previous studies, the researcher came up with a proposed approach that can be applied to some government institutions through accounting requirements. The researcher came up through statistical analysis using the Chi-square test, to indicate the significance of this proposed approach among the selected sample, with an order of priorities. The researcher found out the safety and strength of the proposed approach through the sample answers for many of them. the researcher believes that the application of the proposed approach and the five axes that could be deduced from the answers of the study categories, contributes greatly to the financial discipline to achieve sustainable development for Egypt 2030.

| Published in | Journal of Finance and Accounting (Volume 12, Issue 4) |

| DOI | 10.11648/j.jfa.20241204.12 |

| Page(s) | 87-107 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2024. Published by Science Publishing Group |

Institutional Reform, Digital Transformation, Financial Discipline, Sustainable Development

Years | The value of public debt | Local debt | External debt | Gross domestic product | Ratio of public debt to gross domestic product | GDP growth rate | |

|---|---|---|---|---|---|---|---|

Value in Egyptian pounds trillion | Value in million dollars | ||||||

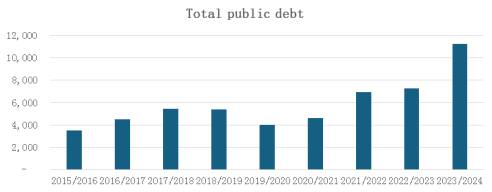

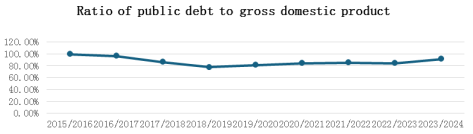

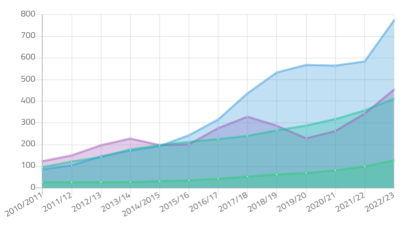

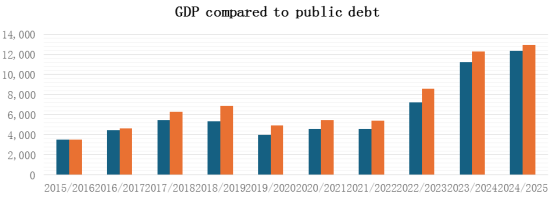

2015/2016 | 3,513 | 2,620 | 0,893 | 55.8 | 3,534 | 99.40% | 4.30% |

2016/2017 | 4,484 | 3,160 | 1,324 | 82.8 | 4,656 | 96.30% | 4.20% |

2017/2018 | 5,435 | 3,696 | 1,739 | 92.8 | 6,312 | 86.10% | 5.30% |

2018/2019 | 5,369 | 4,282 | 1,087 | 108.7 | 6,901 | 77.80% | 5.60% |

2019/2020 | 3,990 | 3,989 | 1,235 | 123.5 | 4,907 | 81.30% | 3.60% |

2020/2021 | 4,592 | 4,591 | 1,378 | 137.9 | 5,453 | 84.20% | 3.30% |

2021/2022 | 4,592 | 5,399 | 1,557 | 155.7 | 5,383 | 85.30% | 6.60% |

2022/2023 | 7,249 | 5,602 | 1,647 | 164.7 | 8,609 | 84.20% | 4.20% |

2023/2024 | 11,241 | 6,018 | 5,223 | 168.5 | 12,312 | 91.30% | 4.10% |

2024/2025 | 12,360 | 6,466 | 5,894 | 125.4 | 12,918 | 95.70% | 4.90% |

Budget target | |||||||

Analysis of 2024/2025 | |

|---|---|

1. Wages and workers’ compensation | 575 |

2. Buy goods and services | 167 |

3. Support, grants, and social benefits | 636 |

4. Other expenses | 162 |

5. Purchasing non-financial assets (investments) | 496 |

Total | 2,036 |

Tax revenues in the general budget in the budget | 2,000 |

First surplus | 36 |

Debt service expenses | 1,834 |

The reality of surplus.........deficit | -1,798 |

Payment of debt instalments | 1,606 |

The reality of the shortage | -3,404 |

Other income | 600 |

The state's general budget deficit | -2,804 |

Sample employers | Study population | Selected sample | Sample responses | Percentage of responses for the selected sample |

|---|---|---|---|---|

An employee of the General Authority for Investment and Free Zones | 350 | 20 | 16 | 80% |

Income tax workers | 150 | 15 | 12 | 80% |

Those working for value-added taxes | 85 | 10 | 8 | 80% |

Workers with wages and salaries taxes | 65 | 10 | 9 | 90% |

Real estate tax workers | 45 | 10 | 6 | 60% |

Freelancers (certified accountants) | 55 | 10 | 10 | 100% |

Total | 750 | 75 | 61 | 81% |

Cronbach’s Alpha | Cronbach's Alpha Based on Standardized Items | N of Items |

|---|---|---|

.955 | .955 | 15 |

| N | Minimum | Maximum | Mean | Std. Deviation | Variance |

|---|---|---|---|---|---|---|

A1 | 61 | 1.00 | 5.00 | 4.5410 | .92329 | .852 |

A2 | 61 | 2.00 | 5.00 | 4.4754 | .88707 | .787 |

A3 | 61 | 1.00 | 5.00 | 4.4098 | 1.00626 | 1.013 |

A4 | 61 | 1.00 | 5.00 | 4.5574 | .80673 | .651 |

A5 | 61 | 1.00 | 5.00 | 4.5410 | .92329 | .852 |

N | Minimum | Maximum | Mean | Std. Deviation | Variance | |

|---|---|---|---|---|---|---|

A6 | 61 | 2.00 | 5.00 | 4.6230 | .73403 | .539 |

A7 | 61 | 1.00 | 5.00 | 4.5410 | .92329 | .852 |

A8 | 61 | 1.00 | 5.00 | 4.2131 | 1.06638 | 1.137 |

A9 | 61 | 1.00 | 5.00 | 4.5082 | .94204 | .887 |

A10 | 61 | 1.00 | 5.00 | 4.4262 | 1.00762 | 1.015 |

N | Minimum | Maximum | Mean | Std. Deviation | Variance | |

|---|---|---|---|---|---|---|

A11 | 61 | 1.00 | 5.00 | 4.5410 | .92329 | .852 |

A12 | 61 | 1.00 | 5.00 | 4.1803 | 1.02483 | 1.050 |

A13 | 61 | 1.00 | 5.00 | 4.5410 | .92329 | .852 |

A14 | 61 | 2.00 | 5.00 | 4.2951 | .91913 | .845 |

A15 | 61 | 2.00 | 5.00 | 4.3279 | .90777 | .824 |

Valid N (listwise) | 61 |

Asymp. Sig. | df | Chi-Square (a, b) | |

|---|---|---|---|

A1 | 0 | 4 | 113.12 |

A2 | 0 | 3 | 60.77 |

A3 | 0 | 4 | 84.656 |

A4 | 0 | 4 | 100.557 |

A5 | 0 | 4 | 113.18 |

A6 | 0 | 3 | 80.574 |

A7 | 0 | 4 | 113.11 |

A8 | 0 | 4 | 54.328 |

A9 | 0 | 4 | 106.459 |

A10 | 0 | 4 | 93.672 |

A11 | 0 | 4 | 113.16 |

A12 | 0 | 4 | 47.443 |

A13 | 0 | 4 | 113.18 |

A14 | 0 | 3 | 33.623 |

A15 | 0 | 3 | 37.154 |

Statistical Ranking | Proposed Approach Item | M |

|---|---|---|

6 | Establishment of tax committees to resolve tax disputes and address customs issues within the premises of investors to facilitate and resolve their problems, particularly in the Egyptian Federation of Industries, the Federation of Chambers of Commerce, and associations of export investors. It is their responsibility to foster trust among stakeholders dealing with government entities, which can only be achieved through immediate response to exporters' requests for export support, VAT credit balances, electronic tax audits, electronic issuance and renewal of import cards, commercial registry amendments, and issuance of tax cards. | 1 |

3 | The necessity of reviewing the performance of the Egyptian revenue authority, including the Egyptian Tax Authority, Real Estate Tax Authority, and Customs Authority, according to the Tax Administration Diagnostic Assessment Tool (TADAT), to provide an objective diagnosis of strengths and weaknesses aiming to achieve international transparency and integrity standards. This includes enhancing their operations, maximizing revenues, and improving the effectiveness of government spending on these institutions. | 2 |

8 | It is essential to engage in effective communication with the International Bureau of Fiscal Documentation (IBFD), an esteemed organization in tax publications, to provide tax awareness services and increase tax interaction with the Federation of Chambers of Commerce, exporters, and the Federation of Industries. This aims to enhance voluntary compliance among taxpayers and prevent excessive intervention by the tax administration during tax audits, particularly for large and medium taxpayers who contribute more than 80% of sovereign revenue | 3 |

2 | لIt is imperative to implement a deficit reduction strategy (targeted in the 2024/2025 budget at 6% of the gross domestic product) through rationalizing government spending and reducing it to 85% of the allocated budget. This includes setting a cap on public debt (domestic and external) at 90% of the gross domestic product for the 2024/2025 budget, with an annual reduction rate of 5%. This will be achieved by investing 10% of the government's loans in separate funds dedicated to repaying long-term debts. | 4 |

6 | Control the annual ceiling of the general government debt not exceeding 60% by the year 2030 and continue maintaining this ceiling annually until it reaches 40% by the year 2040. | 5 |

1 | The introduction of the concept of government budgeting necessitates that government entities undergo review by international auditing institutions, such as the BIG 4 accounting firms, to provide limited audit services and other assurance tasks. This is to ensure that government dealings with the public and financial transactions are conducted directly rather than through intermediaries in Egypt, aiming to achieve international transparency and integrity standards. The auditing firm should be changed annually to correct annual paths in budget implementation, aiming to enhance public spending efficiency and achieve inclusivity in budget execution. | 6 |

6 | It is necessary to provide tax incentives (a 50% deduction from taxable profits in the first five years) similar to those applied in Morocco and Spain, to localize the Egyptian industry in heavy industries such as aircraft, ships, trains, and cars, considering them as strategic priority activities, akin to what was proposed in the Green Hydrogen Law | 7 |

10 | It is imperative to provide loans not exceeding 10% for industrial and agricultural activities, with the Ministry of Finance bearing the differences in interest rates, to reduce the cost of sales. This will reflect in lower selling prices for products, thus achieving market equilibrium between producers and consumers, with strict price monitoring through price radar systems | 8 |

3 | Reviewing and monitoring the implementation of the budget of government entities on a regular basis by the Ministry of Finance's auditors as a pre-disbursement control, along with stating the feasibility of financial expenditures to ensure expenditure seriousness, to implement a balanced path for financial sustainability purposes. | 9 |

8 | Reducing the number of ministries in the state administrative apparatus, taking into consideration the reduction and rationalization of public expenditures, in line with practices followed in the United States and the European Union. Egypt currently has 33 ministries, and for comprehensive institutional reform to be adopted, it is necessary to reduce this number of ministries as well as public bodies. This will be achieved through agreements between the Ministry of Planning and the Central Agency for Organization and Administration, and the establishment of a body to ensure the quality of government services and the implementation of a system of rewards and penalties. | 10 |

6 | Increasing and enhancing internet services and implementing fifth-generation technology electronically to operate all government services remotely, thereby addressing bureaucratic hurdles and administrative corruption. Utilizing financial inclusion tools to activate the electronic provision of all government services and delivering official documents through private sector delivery companies directly to the service recipients within 24 hours at most | 11 |

9 | As a result of the public revenues not keeping pace with public expenditures, it is imperative to reduce public expenditures to enhance overall spending efficiency. | 12 |

6 | Opening new outlets and markets in Africa to boost agricultural and industrial exports is crucial, as it represents a promising market and fertile ground for Egyptian products. Providing support from the government to exporters and removing all obstacles facing export companies is essential. This includes promptly refunding value-added tax on export inputs upon submission of export revenue transfer notices to Egyptian banks | 13 |

5 | Increasing the inclusivity of the tax community, especially the informal sector, is essential for achieving tax justice and attaining a higher tax collection rate from the available tax base. This should reach up to 20% of the gross domestic product, aiming to raise tax revenues to 2.6 trillion. This entails simplifying accounting procedures and extending the application deadline for Article 3 of Law No. 30 of 2023, amending the provisions of Law No. 91 of 2005, the Income Tax Law, to cover all small businesses with annual turnover less than 20 million. Additionally, implementing electronic invoicing across the community to facilitate electronic tax accounting procedures. | 14 |

4 | Considering the decrease in the value of the Egyptian pound against foreign currencies, it is necessary to adjust the tax registration threshold for value-added tax to one million pounds instead of 500,000 pounds. This adjustment encourages society to register and adopt electronic invoicing, with registration becoming mandatory once the threshold is reached. It should be noted that registration is required for all professionals. | 15 |

| [1] | Official Gazette - Issue No. 9 (A) of Year 76, issued on March 3, 2024. |

| [2] | Minister of Investment's Decision No. 110 of the year 2015, issuing Egyptian Accounting Standards. |

| [3] | Luis Alfonso Dau, Elizabeth M. Moore, Tatiana Kostova, “The impact of market based institutional reforms on firm strategy and performance: Review and extension”, Journal of World Business, 3 February 2020. |

| [4] | Jorge Gallego, Stanislao Maldonado, Lorena Trujillo, “From curse to blessing? institutional reform and resource booms in Colombia”. Journal of Economic Behavior & Organization,10 August 2020. |

| [5] | Oliver Hülsewig, Armin Steinbach, “Monetary financing and fiscal discipline”. International Review of Law and Economics, 2 July 2021. |

| [6] | André Carlos Busanelli de Aquino, Richard A. Batley, “Pathways to hybrid-ization: Assimilation and accommodation of public financial reforms in Brazil”. Accounting, Organizations and Society, 8 September 2021. |

| [7] | Rosaria Rita Canale, Elina De Simone, Nicola Spagnolo, “Financial markets and fiscal discipline in the Eurozone”, Structural Change and Economic Dynamics, 25 July 2021. |

| [8] | Vasvári, Tamas, “Hardening the budget constraint: Institutional reform in the financial management of Hungarian local governments”. Business & Economics Journal, Volume70 Issue4, 2021. |

| [9] | Shivani Narayan, Dilip Kumar, Elie Bouri, “Systemically important financial institutions and drivers of systemic risk: Evidence from India”, Pacific-Basin Finance Journal, 17 September 2023. |

| [10] | Antonio A. Golpe, A. Jesus Sánchez-Fuentes, José Carlos Vides, “Fiscal sustainability, monetary policy, and economic growth in the Euro Area: In search of the ultimate causal path”. Economic Analysis and Policy, 8 May 2023. |

| [11] | Muhammad Lotfy Youssef Nasr; Mr. Hassan Mahdi Amer: “Institutional change and possibilities for improving water management in light of economic reform policies in the Arab Republic of Egypt,” Egyptian Journal of Development and Planning, Volume 6, Issue 1, June: 1998. |

| [12] | Asmaa Ezzat: “Institutional reform and governance as a basic pillar for building the new Egyptian state,” International Journal of Public Policy in Egypt, Volume 2 – Issue 3, July: 2023. |

| [13] | Muhammad Lotfy Youssef Nasr; Mr. Hassan Mahdi Amer: “Institutional change and possibilities for improving water management in light of economic reform policies in the Arab Republic of Egypt,” Egyptian Journal of Development and Planning, Volume 6, Issue 1, June: 1998. |

| [14] | Jin Zhao, Ghulam Rasool Madni, “Institutional Reforms and Their Impact on Economic Growth and Investment in Developing Countries” School of Finance, Shanghai Lixin University of Accounting and Finance, Shanghai, China: 2019. |

| [15] | Chen ChenTian ZhangXiulin Qi, “Regional financial reform and corporate green innovation–Evidence based on the establishment of China National Financial Comprehensive Reform Pilot Zones”. Finance Research Letters, 12 December 2023. |

| [16] | Hongguang Sui Simin Geng Noshaba Aziz, “Fiscal institutional reform and export product quality: Quasi-experimental research on counties managed directly by provinces” Economic Modelling, 27 May 2023. |

| [17] | Mohamedeen Sayed Ahmed, 2020, “Egypt’s Dream 2030, Paperless Gov-ernment, “Digital Transformation” is a Quantitative Shift that Liberates Egypt from Bureaucracy and Administrative Corruption,” Arab Business Administration Association, Year: 2020, Issue, 170, p. 6. |

| [18] | The state's general budget 2024/2025. |

| [19] | MIT Sloan Management Review, |

| [20] | Investment Authority website |

| [21] | Information Sector at the Egyptian Tax Authority |

| [22] | Mohamed Amin Hanafi Abdullah, Mechanisms of Digital Transformation and Financial Discipline (Case Study: India). Scientific Journal of Business Research, Faculty of Commerce - Menoufia University. Volume 49, Issue 2, Part 1 (April: 2023) |

| [23] | Official Gazette, Law No. 18 of 2024, Issue No. 13, repeated (1), issued on 30/3/2024 |

| [24] | The Official Gazette, Law No. (6) for the year 2022, Issue No. (5) reissued (d), issued on February 8, 2022. |

| [25] | Nasserine Fayez Ahmed Bedawi: "Financial Discipline and its Impact on Public Debt in Egypt," Scientific Journal of Research and Business Studies, Issue No. (37), June 2023. |

| [26] | The Official Gazette, Issue No. (9) repeated (a), Prime Minister's Decision No. (636) of the year 2024, issued on March 3, 2024. |

| [27] | The General Budget of the Egyptian State 2024/2025. |

APA Style

Ebrahim, N. A. E. R., Mohamed, A. H. (2024). Accounting Requirements for Institutional Reform to Achieve Egypt’s Vision 2030 for Sustainable Financial Discipline, Proposed Approach. Journal of Finance and Accounting, 12(4), 87-107. https://doi.org/10.11648/j.jfa.20241204.12

ACS Style

Ebrahim, N. A. E. R.; Mohamed, A. H. Accounting Requirements for Institutional Reform to Achieve Egypt’s Vision 2030 for Sustainable Financial Discipline, Proposed Approach. J. Finance Account. 2024, 12(4), 87-107. doi: 10.11648/j.jfa.20241204.12

AMA Style

Ebrahim NAER, Mohamed AH. Accounting Requirements for Institutional Reform to Achieve Egypt’s Vision 2030 for Sustainable Financial Discipline, Proposed Approach. J Finance Account. 2024;12(4):87-107. doi: 10.11648/j.jfa.20241204.12

@article{10.11648/j.jfa.20241204.12,

author = {Nabil Abd El Raouf Ebrahim and Aber Hany Mohamed},

title = {Accounting Requirements for Institutional Reform to Achieve Egypt’s Vision 2030 for Sustainable Financial Discipline, Proposed Approach

},

journal = {Journal of Finance and Accounting},

volume = {12},

number = {4},

pages = {87-107},

doi = {10.11648/j.jfa.20241204.12},

url = {https://doi.org/10.11648/j.jfa.20241204.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jfa.20241204.12},

abstract = {The digital transformation in Egypt derives, its importance from the Sustainable Development Goals (Egypt Vision 2030) to reduce borrowing in addition to reducing public debt and the sustainability of financial inclusion, and this is achieved through financial discipline, which is one of the most prominent topics that have received wide attention in many developed countries, perhaps the accounting requirements to achieve institutional reform contributes greatly to financial discipline, especially with financial inclusion, especially when preparing the public budget in order to measure the ability of public expenditure to achieve sustainable development indicators, from the ability to manage financial expenditure, and revenues accurately and in a way that responds to financial goals after reviewing the previous studies, the researcher came up with a proposed approach that can be applied to some government institutions through accounting requirements. The researcher came up through statistical analysis using the Chi-square test, to indicate the significance of this proposed approach among the selected sample, with an order of priorities. The researcher found out the safety and strength of the proposed approach through the sample answers for many of them. the researcher believes that the application of the proposed approach and the five axes that could be deduced from the answers of the study categories, contributes greatly to the financial discipline to achieve sustainable development for Egypt 2030.

},

year = {2024}

}

TY - JOUR T1 - Accounting Requirements for Institutional Reform to Achieve Egypt’s Vision 2030 for Sustainable Financial Discipline, Proposed Approach AU - Nabil Abd El Raouf Ebrahim AU - Aber Hany Mohamed Y1 - 2024/09/26 PY - 2024 N1 - https://doi.org/10.11648/j.jfa.20241204.12 DO - 10.11648/j.jfa.20241204.12 T2 - Journal of Finance and Accounting JF - Journal of Finance and Accounting JO - Journal of Finance and Accounting SP - 87 EP - 107 PB - Science Publishing Group SN - 2330-7323 UR - https://doi.org/10.11648/j.jfa.20241204.12 AB - The digital transformation in Egypt derives, its importance from the Sustainable Development Goals (Egypt Vision 2030) to reduce borrowing in addition to reducing public debt and the sustainability of financial inclusion, and this is achieved through financial discipline, which is one of the most prominent topics that have received wide attention in many developed countries, perhaps the accounting requirements to achieve institutional reform contributes greatly to financial discipline, especially with financial inclusion, especially when preparing the public budget in order to measure the ability of public expenditure to achieve sustainable development indicators, from the ability to manage financial expenditure, and revenues accurately and in a way that responds to financial goals after reviewing the previous studies, the researcher came up with a proposed approach that can be applied to some government institutions through accounting requirements. The researcher came up through statistical analysis using the Chi-square test, to indicate the significance of this proposed approach among the selected sample, with an order of priorities. The researcher found out the safety and strength of the proposed approach through the sample answers for many of them. the researcher believes that the application of the proposed approach and the five axes that could be deduced from the answers of the study categories, contributes greatly to the financial discipline to achieve sustainable development for Egypt 2030. VL - 12 IS - 4 ER -

High Institute for Computers, and Information Technology, Sherouk Academy, Cairo, Egypt

High Institute for Computers, and Information Technology, Sherouk Academy, Cairo, Egypt

Figure 1. The Interrelation between the Axes of Digital Transformation.

Figure 2. The Importance of Financial Discipline in Financial Planning.

Figure 3. Financial Discipline is Essential for Financial Success.

Figure 4. The Importance of Financial Discipline in Controlling Inflation.

Figure 5. Development of total public debt during the years of study.

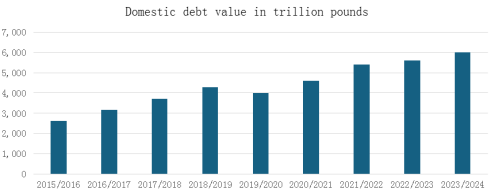

Figure 6. The development of internal debt during the years of study.

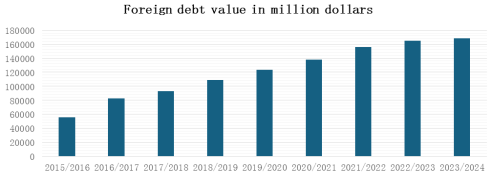

Figure 7. Development of foreign debt during the years of study.

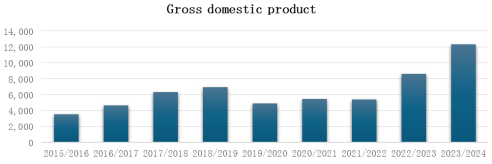

Figure 8. Development of GDP during the years of study.

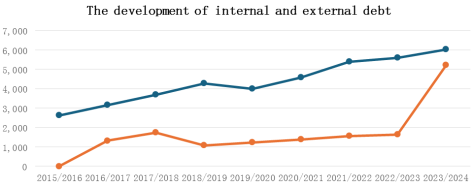

Figure 9. Development of internal and external debt during the years of study.

Figure 10. Development of the ratio of public debt to GDP during the years of study

Figure 11. Interest, support, and wage payments during the years of study.

Figure 12. GDP compared to public debt (value in trillion pounds).