1. Introduction

Financial institutions serve as vital intermediaries in the economy, facilitating transactions between lenders and borrowers. Banks, being primary financial intermediaries, play a crucial role in bridging the funding gap between surplus and deficit units, thereby fostering economic growth by directing capital from savers to borrowers

| [27] | Hussen, A, R & Habtamu A, L, “Factors Determining Banks’ Loan and Advance: A Case Study on Commercial Banks in Ethiopia,” Journal of Finance and Accounting 11/3 (2023), 113–123. |

| [24] | Habtamu A, L, & Zemenu F. Determinants of Commercial Banks Credit Growth in Case of Ethiopian Commercial Banks. IISTE Developing country studies. Vol 11 No 2, 2021. |

[27, 24]

. In developing economies, commercial banks encounter various risks during the lending process, which can significantly impact their profitability and even lead to institutional closures. Among these risks, credit risk stands out as a primary threat to the financial performance of banks

| [8] | Bhattarai, B. P. (2020). Effects of Non-performing Loan on Profitability of Commercial Banks in Nepal, European Business & Management. 6(6), 164-170. https://doi.org/10.11648/j.ebm.20200606 |

| [22] | Fiedler, E. R. (1971). The meaning and importance of Credit Risk. In Measures of Credit Risk and Experience (pp. 10- 18). NBER. |

| [25] | Habtamu A, L, & Zemenu F. Determinants of Banks Liquidity: In Case of Commercial Banks in Ethiopia. Research journal of Finance and Accounting. DOI: 10.7176/RJFA/13-8-06. Vol 13, No 8 (2022) |

| [39] | National Bank of Ethiopia. (2007). Asset Classification and Provisioning, Directive No. SBB/43/2007. |

| [51] | Sianturi, C., & Rahadian, D. (2020). Analysis of The Effect of Capital Adequacy Ratio (CAR), Non-Performing Loan (NPL), Net Interest Margin (NIM), Operating Expenses to Operating Income (BOPO), and Loan to Deposit Ratio (LDR) on Profitab. International journal of scientific and research publications, 10, 758-768. |

| [61] | Zergaw, F. (2015). Determinants of micro finance profitability: the case of selected micro finance institutions. Jimma University 90. Jimma: Jimma University. |

[8, 22, 25, 39, 51, 61]

. Effective credit risk management is imperative for commercial banks to maintain profitability and ensure their long-term viability. Banks can mitigate potential losses and enhance their financial stability by closely monitoring and managing credit risk. In the face of evolving market conditions and economic uncertainties, robust risk management practices become even more critical for financial institutions

| [2] | Ahmadyan, A. (2018). Measuring credit risk management and its impact on bank performance in Iran. Marketing and Branding Research, 5, 168-183. |

| [19] | Deyganto, K. O. (2020). The Assessing Credit Risk Management Practice of MFIs: Evidence from Micro Finance Institutions in Sidama Regional State, Ethiopia. |

| [36] | Mulugeta, W. (2016). The Impact of Credit Risk Management on Performance of Banks. The Case Study of Selected Commercial Banks in Ethiopia (Doctoral dissertation). |

| [41] | National Bank of Ethiopia (2013), Reserve Requirement, 6th Replacement Directive No. SBB/55/2013. |

| [48] | Popa, G, Mihallescu, Land Caragea, C (2009), 'EVA - Advanced method for performance evaluation in banks', Economia Seria management Journal, Vol.12, No.1, pp.268-173. |

| [51] | Sianturi, C., & Rahadian, D. (2020). Analysis of The Effect of Capital Adequacy Ratio (CAR), Non-Performing Loan (NPL), Net Interest Margin (NIM), Operating Expenses to Operating Income (BOPO), and Loan to Deposit Ratio (LDR) on Profitab. International journal of scientific and research publications, 10, 758-768. |

[2, 19, 36, 41, 48, 51]

.

The focus on credit risk management is not only essential for individual banks but also holds broader implications for the overall health of the financial sector and the economy at large. Sound risk management practices help to safeguard financial stability, build resilience against external shocks, and promote sustainable economic growth

| [5] | Ajayi, S. O., Ajayi, H. F., Enimola, D. J., & Orugun, F. I. (2019). Effect of Capital Adequacy Ratio (CAR) on Profitability of Deposit Money Banks (DMB’s): A Study of DMB’s with International Operating License in Nigeria. Research Journal of Finance and Accounting, 10 (10), 84-91. |

| [13] | Brooks, C. (2008). Introductory Econometrics of Finance, 2nd ed., the ICMA Center, University of Reading, CAMBRIDGE University press. |

| [16] | Dvorský, J., Schönfeld, J., Kotásková, A., & Petráková, Z. (2018). Evaluation of Important Credit Risk Factors in the SME Segment. The Journal of international studies, 11, 204-216. |

| [23] | Habtamu A, L, Hussen A, R & Semira J. Internal Audit Effectiveness and Its Determinant Factors in Commercial Banks of Ethiopia: The Case of Bale Robe Town. International Journal of Accounting, Finance and Risk Management. Volume 8, Issue 2, June 2023, pp. 49-56. https://doi.org/10.11648/j.ijafrm.20230802.13. |

[5, 13, 16, 23]

. Therefore, emphasizing the importance of effective credit risk management is crucial not only for the success of individual financial institutions but also for the stability and growth of the broader economy. Bank credit plays a crucial role in providing essential financial support to various sectors such as households, businesses, and governments. However, this process of creating credit exposes banks to significant default risks, which can lead to financial difficulties and potential insolvency

| [1] | Abdirahman, A. (2015). Impact Of Credit Risk Management on Financial Performance of Ethiopian Microfinance Institutions: The Case Study Of Somali Microfinance Institution Share Company (Doctoral dissertation, ASTU). |

| [7] | Asutay, M., & Izhar, H. (2007). Estimating the profitability of Islamic banking: evidence from bank Muamalat Indonesia. Review of Islamic Economics, 11(2), 17-29. |

| [45] | Olabamiji, O., & Michael, O. (2018). Credit management practices and bank performance: Evidence from First Bank. South Asian Journal of Social Studies and Economics, 1-10. |

| [33] | Margaritis, T. (2010). Evaluation of Credit risk based on financial performance, Europian journal of operational research. |

| [58] | Treacy, W. F., & Carey, M. (2000). Credit risk rating systems at large US banks. Journal of Banking & Finance, 24(1-2), 167-201. |

| [60] | Zaidi, F. B., & Sarwar, A. (2013). Design and Development of Credit Scoring Model for the Commercial Banks in Pakistan: Forecasting Creditworthiness of Corporate Borrowers Asia. |

[1, 7, 45, 33, 58, 60]

.

Setting credit standards for borrowers plays a critical role in determining the financial health of banks. The primary objective of credit risk management is to reduce the impact of risks on commercial banks and other businesses

| [2] | Ahmadyan, A. (2018). Measuring credit risk management and its impact on bank performance in Iran. Marketing and Branding Research, 5, 168-183. |

| [19] | Deyganto, K. O. (2020). The Assessing Credit Risk Management Practice of MFIs: Evidence from Micro Finance Institutions in Sidama Regional State, Ethiopia. |

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

| [51] | Sianturi, C., & Rahadian, D. (2020). Analysis of The Effect of Capital Adequacy Ratio (CAR), Non-Performing Loan (NPL), Net Interest Margin (NIM), Operating Expenses to Operating Income (BOPO), and Loan to Deposit Ratio (LDR) on Profitab. International journal of scientific and research publications, 10, 758-768. |

[2, 19, 34, 51]

. Given that loans form a significant part of the financial activities of commercial banks, they are inherently exposed to credit risks. Therefore, commercial banks need to have a robust credit risk management system in place to ensure their continued viability

| [31] | Nwosi, A. A. (2015). Asset Quality and Profitability of Commercial Banks: Evidence from Nigeria. Research Journal of Finance and Accounting, 6, 26-34. |

| [54] | Shmendi, A. (2019). The Impact Of Credit Risk Management On Financial Performance Commercial Banks Of Ethiopia (Doctoral dissertation). |

[31, 54]

. Commercial banks are instrumental in mobilizing financial resources for investments by providing credit facilities to firms and investors. The primary revenue sources for banks often come from the interest earned on loans and advances. However, offering lending services exposes banks to various risks, including liquidity and credit risks. Mitigating these risks through effective risk management practices is crucial for the stability and sustainability of financial institutions and the broader financial ecosystem

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [39] | National Bank of Ethiopia. (2007). Asset Classification and Provisioning, Directive No. SBB/43/2007. |

| [45] | Olabamiji, O., & Michael, O. (2018). Credit management practices and bank performance: Evidence from First Bank. South Asian Journal of Social Studies and Economics, 1-10. |

| [51] | Sianturi, C., & Rahadian, D. (2020). Analysis of The Effect of Capital Adequacy Ratio (CAR), Non-Performing Loan (NPL), Net Interest Margin (NIM), Operating Expenses to Operating Income (BOPO), and Loan to Deposit Ratio (LDR) on Profitab. International journal of scientific and research publications, 10, 758-768. |

[34, 37, 39, 45, 51]

.

Credit risk management should be at the center of bank operations to maintain financial sustainability and reach more clients. Numerous researchers have studied the subject and come to various conclusions. Several studies in different countries across the world and concluded that credit risk management has a significant influence on the profitability of banks

| [3] | Aschis, G. (2016). The Impact Of Credit Risk On Financial Performance Of Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [11] | Biruk, D. (2015). Assessment of credit risk management practice of commercial bank of Ethiopia (Doctoral dissertation, St. Mary's University). |

| [12] | Bluhm, C., Overbeck, L., & Wagner, C. (2016). Introduction to credit risk modeling. Crc Press. |

| [21] | Flamini, V., McDonald, C., and Schumacher, L., (2009). The determinants of commercial bank profitability in Sub Saharan Africa IMF Working Paper, 09/15(january), 1-30. |

| [35] | Million, G., Matewos, K., & Sujata, S. (2015). The impact of credit risk on profitability performance of commercial banks in Ethiopia. African Journal of Business Management, 9, 59-66. |

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [46] | Poudel, R. P. (2012). The impact of credit risk management on financial performance of commercial banks in Nepal. International Journal of Arts and Commerce, 1 (5), 9-15. |

| [53] | Sari, L., & Septiano, R. (2020). Effects of Intervening Loan to Deposit Ratio On Profitability. |

| [57] | Tadesse, E. (2014). Impact of credit risk on the performance of commercial banks in Ethiopia (Doctoral dissertation, St. Mary's University). |

[3, 11, 12, 21, 35, 37, 46, 53, 57]

.

For instance, using loan default monitoring, credit scoring, credit polices and procedure as credit risk management indicators to measure performance of bank

| [18] | Elgari, M. A. (2003). Credit risk in Islamic banking and finance. Islamic Economic Studies, 10(2). |

[18]

. In Nigeria using interest risk, capital adequacy risk and credit risk as credit risk management dimensions, to measure the bank's performance

| [27] | Hussen, A, R & Habtamu A, L, “Factors Determining Banks’ Loan and Advance: A Case Study on Commercial Banks in Ethiopia,” Journal of Finance and Accounting 11/3 (2023), 113–123. |

| [32] | Lee, K., Su, W., & Liu, C. (2017). Operating Performance Evaluation Based on Z-score Model and Profitability between Cross-Straits Credit Cooperatives. Review of Economics and Finance, 10, 72-82. |

[27, 32]

. From Ethiopia few researchers also conducted on the same area by using micro economic and macro-economic variable (capital adequacy ratio, loan to deposit ratio, loan growth ratio, unemployment rate, GDP, inflation, loan loss provision, and non-performance ratio)

| [35] | Million, G., Matewos, K., & Sujata, S. (2015). The impact of credit risk on profitability performance of commercial banks in Ethiopia. African Journal of Business Management, 9, 59-66. |

| [36] | Mulugeta, W. (2016). The Impact of Credit Risk Management on Performance of Banks. The Case Study of Selected Commercial Banks in Ethiopia (Doctoral dissertation). |

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [3] | Aschis, G. (2016). The Impact Of Credit Risk On Financial Performance Of Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [57] | Tadesse, E. (2014). Impact of credit risk on the performance of commercial banks in Ethiopia (Doctoral dissertation, St. Mary's University). |

| [54] | Shmendi, A. (2019). The Impact Of Credit Risk Management On Financial Performance Commercial Banks Of Ethiopia (Doctoral dissertation). |

| [11] | Biruk, D. (2015). Assessment of credit risk management practice of commercial bank of Ethiopia (Doctoral dissertation, St. Mary's University). |

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

[35-37, 3, 57, 54, 11, 34]

.

Hence, the preceding research in Ethiopia lacked an exploration of the literature gap by omitting the inclusion of credit interest income ratio and asset growth ratio as explanatory variables in their analyses. Furthermore, it was noted that several researchers utilized the same variable for both independent and dependent variables, leading to contradictory findings. Therefore, this study distinguishes itself from previous research endeavors by seeking to address the gap in variable inclusion. It does so by introducing credit interest income ratio and cost per loan assets ratio as additional independent variables. The primary objective of this study is to investigate the impact of credit risk management indicators, including non-performing loans ratio, interest coverage ratio, loan loss provision ratio, loan-to-deposit ratio, capital reserve ratio, loan-to-asset ratio, and cost per loan assets ratio, on the profitability of selected commercial banks spanning from 2011 to 2023G. C. The aim is to provide valuable insights for policymakers by examining the specific effects of each variable on the profitability of commercial banks in Ethiopia.

1.1. Objective of the Study

The main of the study was to find out the impact of credit risk management on the financial performance of commercial banks in Ethiopia.

1.2. Hypothesis of the Study

The study's hypotheses are based on previous empirical research on commercial bank lending as well as credit risk theories that various academics have developed throughout time. The expectations for the relationship between credit risk and profitability indicators were based on the assumptions established from the literature review. The current study therefore aims to evaluate the seven hypotheses listed below in light of its objective:

Ha1 - Non-performing loans (NPL) has significant negative effect on Return on Asset (ROA).

Ha2-Credit Interest income ratio (CIR) has significant positive effect on Return on Asset (ROA).

Ha3 –Loan loss provision (LLP) has significant negative effect on Return on Asset (ROA).

Ha4-Loan to deposit ratio has significant negative effect on Return on Asset (ROA).

Ha5-Capital Adequacy ratio (CAR) has significant positive effect on Return on Asset (ROA).

Ha6- Loan to asset ratio has significant positive effect on Return on Asset (ROA).

Ha7- operational cost efficiency (OCE) has significant negative effect on Return on Asset (ROA).

2. Literature Review

Risk management in the financial realm is vital for mitigating the variability between anticipated and actual returns associated with investments. It encompasses the identification of key risk areas, establishment of thresholds, development of mitigation strategies, and consistent monitoring to uphold risk levels within manageable bounds

| [10] | Bekele, B. (2015). The Nexus between Bank Specific Risk Management Practice and Financial Performance: A Study on Selected Commercial Banks in Ethiopia. Available at SSRN 2841206. |

[10]

. Despite the inherent challenges in precisely quantifying risks, banks worldwide are increasingly incorporating robust risk management practices into their operations, largely driven by regulatory mandates that emphasize the importance of risk mitigation for financial stability

| [24] | Habtamu A, L, & Zemenu F. Determinants of Commercial Banks Credit Growth in Case of Ethiopian Commercial Banks. IISTE Developing country studies. Vol 11 No 2, 2021. |

[24]

.

According to

| [36] | Mulugeta, W. (2016). The Impact of Credit Risk Management on Performance of Banks. The Case Study of Selected Commercial Banks in Ethiopia (Doctoral dissertation). |

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [44] | Ozili, P. (2017). Bank Profitability and Capital Regulation: Evidence from Listed and non-Listed Banks in Africa. Journal of African Business, 18, 143 - 168. |

| [47] | Pesaran, M. H., Schuermann, T., Treutler, B. J., & Weiner, S. M. (2006). Macroeconomic dynamics and credit risk: a global perspective. Journal of Money, Credit and Banking, 1211-1261. |

| [51] | Sianturi, C., & Rahadian, D. (2020). Analysis of The Effect of Capital Adequacy Ratio (CAR), Non-Performing Loan (NPL), Net Interest Margin (NIM), Operating Expenses to Operating Income (BOPO), and Loan to Deposit Ratio (LDR) on Profitab. International journal of scientific and research publications, 10, 758-768. |

| [59] | Tenriola, A. (2019). Anteseden Return on Asset (ROA) pada Bank BUMN Indonesia. Unuafe, O. K. (2013). Impact of Credit Risk Management and Capital Adequacy on the Financial Performance of Commercial. |

[36, 37, 44, 47, 51, 59]

Financial institutions, including banks, confront a spectrum of risks such as credit, liquidity, market, operational, reputation, and legal risks, each capable of exerting significant impacts on their operations and financial health. Among these, credit risk stands out as a pervasive threat, involving the potential default of counterparties in loan or derivative transactions. Recognized as a cornerstone of prudent banking practices, managing credit risk is essential for a bank's survival. While liquidity, interest rate, foreign exchange, and credit risks are commonly acknowledged as critical elements in risk management, understanding credit default is paramount in gauging a bank's overall credit risk exposure

| [50] | Rex, U. (2016). Loan Risk (LR), Loan Risk Management (LRM) and Commercial Bank Profitability: A Panel Analysis of Nigerian Banks. |

[50]

.

2.1. Credit Risk

The essence of credit risk lies in the possibility that a borrower or counterparty may not fulfill their obligations as agreed with a bank, posing potential financial losses. Effective credit risk management aims to optimize a bank's risk-adjusted returns by keeping credit risk exposure at acceptable levels

| [40] | National Bank of Ethiopia (2010), Revised Risk Management Guidelines, Bank Supervision Directorate. |

[40]

. Banks must navigate credit risks across their entire portfolio and individual transactions, considering their interplay with other forms of risk. The adept handling of credit risk is indispensable within a broader risk management strategy, playing a pivotal role in the sustained success of banking institutions

| [41] | National Bank of Ethiopia (2013), Reserve Requirement, 6th Replacement Directive No. SBB/55/2013. |

| [56] | Tamrat, W. (2015). Credit Risk Management And Its Impact On Financial Performance Of Ethiopian Private Commercial Banks (Doctoral dissertation, ASTU). |

[41, 56]

.

Credit risk revolves around the threat of financial loss stemming from a debtor's failure to meet obligations to the bank as per the agreed terms

| [28] | Idowu Abiola. (2014). The impact of credit risk management on the development banks performance in Nigeria, International Journal of Management and Sustainability. |

| [39] | National Bank of Ethiopia. (2007). Asset Classification and Provisioning, Directive No. SBB/43/2007. |

[28, 39]

. It is closely tied to traditional lending activities, manifesting as the risk of loans not being repaid fully or partially. Default risk underscores the uncertainty that the anticipated cash flows from loans and securities may not materialize entirely, jeopardizing both the principal lent and the expected interest payments

| [41] | National Bank of Ethiopia (2013), Reserve Requirement, 6th Replacement Directive No. SBB/55/2013. |

[41]

. This type of risk, inherent in lending, encompasses the potential repercussions of a borrower's failure to meet payment obligations, encompassing lost principal, disrupted cash flows, and escalated collection expenses. Effective credit risk management is a linchpin in the operational success and resilience of banking entities, necessitating a holistic approach to risk oversight to safeguard against potential financial pitfalls

| [3] | Aschis, G. (2016). The Impact Of Credit Risk On Financial Performance Of Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [10] | Bekele, B. (2015). The Nexus between Bank Specific Risk Management Practice and Financial Performance: A Study on Selected Commercial Banks in Ethiopia. Available at SSRN 2841206. |

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [46] | Poudel, R. P. (2012). The impact of credit risk management on financial performance of commercial banks in Nepal. International Journal of Arts and Commerce, 1 (5), 9-15. |

[3, 10, 37, 46]

.

2.2. The Source of Credit Risk & Its Management

According to

| [4] | Annor, E. S., & Obeng, F. S. (2017). Impact of credit risk management on the profitability of selected commercial banks listed on the Ghana stock exchange. Journal of Economics, Management and Trade. |

[4]

, Credit risk arises from a multitude of factors originating internally and externally. Internally, deficiencies in credit policy, poor borrower financial assessments, excessive reliance on collateral, and inadequate post-sanction monitoring contribute significantly to credit risk. Moreover, incentives for bank employees can lead to moral hazards and suboptimal lending decisions. Externally, economic conditions, unemployment rates, inflation, interest rate fluctuations, and regulatory environments all play substantial roles in amplifying credit risk. Effective credit risk management is essential for financial institutions to navigate these complexities

| [42] | Nguyen, T. H. (2020). Impact of Bank Capital Adequacy on Bank Profitability under Basel II Accord: Evidence from Vietnam. Journal of economic development, 45, 31-46. |

| [7] | Asutay, M., & Izhar, H. (2007). Estimating the profitability of Islamic banking: evidence from bank Muamalat Indonesia. Review of Islamic Economics, 11(2), 17-29. |

[42, 7]

. Mitigating credit risk involves not only securing loans and managing risks but also ensuring that loans are repaid in full and on time. Institutions proficient in minimizing nonperforming loans tend to fare better financially and ensure long-term sustainability. Overworked personnel within banks can lead to poor credit appraisal systems, financial crimes, and a buildup of low-quality assets, underscoring the need for robust risk management practices. Understanding and addressing the diverse sources of credit risk is crucial for maintaining financial stability and resilience in the banking sector

| [9] | Ball, R., Gerakos, J., Linnainmaa, J. T., & Nikolaev, V. V. (2015). Deflating profitability. Journal of Financial Economics, 117(2), 225-248. |

| [31] | Nwosi, A. A. (2015). Asset Quality and Profitability of Commercial Banks: Evidence from Nigeria. Research Journal of Finance and Accounting, 6, 26-34. |

| [56] | Tamrat, W. (2015). Credit Risk Management And Its Impact On Financial Performance Of Ethiopian Private Commercial Banks (Doctoral dissertation, ASTU). |

[9, 31, 56]

.

Credit risk management is a pivotal practice for financial institutions, involving the assessment of a bank's capital and reserves to mitigate potential losses, a task historically challenging for banks globally. Central to this process is the effective identification, measurement, monitoring, and control of credit risks within a bank's operations, as underscored by the National Bank of Ethiopia. This management approach necessitates a holistic view that encompasses the entire portfolio, individual transactions, and the interplay of credit risk with other forms of risk, emphasizing the need to minimize adverse impacts on earnings and capital. Recognizing that credit risk extends beyond loans to encompass various assets and activities, both on and off-balance sheet, institutions can fortify their financial resilience by implementing robust credit risk management strategies in line with regulatory guidelines and best practices

| [2] | Ahmadyan, A. (2018). Measuring credit risk management and its impact on bank performance in Iran. Marketing and Branding Research, 5, 168-183. |

| [8] | Bhattarai, B. P. (2020). Effects of Non-performing Loan on Profitability of Commercial Banks in Nepal, European Business & Management. 6(6), 164-170. https://doi.org/10.11648/j.ebm.20200606 |

| [13] | Brooks, C. (2008). Introductory Econometrics of Finance, 2nd ed., the ICMA Center, University of Reading, CAMBRIDGE University press. |

[2, 8, 13]

.

Credit Risk Control Tools: Banks in developing countries deploy various tools to control credit losses, including covenants, collateral, credit rationing, loan securitization, and loan syndication.

| [23] | Habtamu A, L, Hussen A, R & Semira J. Internal Audit Effectiveness and Its Determinant Factors in Commercial Banks of Ethiopia: The Case of Bale Robe Town. International Journal of Accounting, Finance and Risk Management. Volume 8, Issue 2, June 2023, pp. 49-56. https://doi.org/10.11648/j.ijafrm.20230802.13. |

[23]

, emphasize that effective risk management hinges largely on qualified personnel and their interactions, with technology serving as a supportive tool. Exposure ceilings play a crucial role in credit risk management, linking prudential limits to capital funds and stipulating thresholds to limit exposures. Review and renewal processes are structured with multi-tier credit approving authorities, delegated powers based on customer ratings, and defined benchmarks for fresh exposures. Risk rating models establish scoring systems and periodic reviews to estimate expected losses and manage rating migrations. Scientific loan pricing ties interest rates to expected losses, ensuring high-risk borrowers face higher costs. Portfolio management strategies optimize diversification benefits and mitigate concentration risks by setting exposure limits across rating categories and industries. Additionally, loan review mechanisms, conducted independently of credit operations, monitor compliance, risk ratings, and signal early warnings for corrective actions, covering a significant portion of the loan portfolio annually to track major credit risks effectively.

2.3. Credit Risk Measurement Framework

The credit risk measurement framework distinguishes between expected loss (EL) and unexpected loss (UL), where EL is considered a cost of business and UL represents the volatility around EL, particularly during economic cycles

| [6] | Akula, R. (2020). Impact Of Non Performing Assets On Profitability - A Study Of Andhra Bank. Aprianti, S. (2018). Pengaruh Kualitas Aktiva Produktif (Kap) Dan Loan to Deposit Ratio (Ldr) Terhadap Profitabilitas (Roa) Pada Pt. Bank Bjb, Tbk Periode 2009-2013. |

[6]

. Credit portfolio models quantify this volatility driven by concentration and correlation factors, with concentration reflecting portfolio risk distribution and correlation indicating responses to macroeconomic shifts. Two valuation approaches, the loss-based method and the NPV-based method, are commonly used. The loss-based method assumes exposures are held to maturity, focusing on repayment or default scenarios without considering credit migration effects. Conversely, the NPV-based method values exposures based on potential upgrades or downgrades, using market spreads or modeling techniques like CAPM. While NPV-based methods suit bond and large corporate portfolios with active markets, loss-based methods are favored for most commercial bank exposures due to simplicity and data requirements. Some institutions implement both methods simultaneously, particularly for securitize portfolios, to enhance credit risk understanding and management effectively

| [14] | Datta, C., & Mahmud, A. (2018). Impact of Capital Adequacy on Profitability Under Basel II Accord: Evidence from Commercial Banks of Bangladesh. European Journal of Business and Management, 10 (8), 48-58. |

| [20] | Doyran, M. A. (2012). Evidence on US Savings and Loan Profitability in Times of Crisis. The International Journal of Business and Finance Research, 6, 35-50. |

| [29] | Kargi, H. S. (2011). Credit risk and the performance of Nigerian banks. Ahmadu Bello University, Zaria. |

| [30] | Koulafetis, P. (2017). Chapter 5: Credit Risk Assessment of Structured Finance Securities. Lucky, L., & |

| [43] | Nwanyanwu, L. A. (2014). Cost of Loan Capital and Capital Asset Acquisition in Nigeria: Implications on Organisational Profitability. European Journal of Business and Management, 6, 199-208. |

[14, 20, 29, 30, 43]

.

2.4. Empirical Literature

Idowu assessed the effect of credit risk on financial performance of commercial banks. The study covered the period between year 2005 and 2014. Credit risk was measured by capital to risk weighted assets, asset quality, loan loss provision, loan and advance ratios and financial performance by return on equity (ROE). The study used the balance sheets components and financial ratios for commercial banks in Kenya registered by year 2014. From the results credit risk has a negative and significant relationship with bank profitability. Poor asset quality or high non-performing loans to total asset is related to poor bank performance both in short run and long run

| [28] | Idowu Abiola. (2014). The impact of credit risk management on the development banks performance in Nigeria, International Journal of Management and Sustainability. |

[28]

.

Mulugeta was conducting its study on examining the impact of credit risk management on the financial performance of private commercial banks in Ethiopia. The study used Random effect panel regression with used for the data of eight private commercial banks in Ethiopia for the sample covered the period from 2007 to 2016. Return on Asset and Return on Equity were dependent variables while non performing loan, capital adequacy, bank size, leverage ratio, credit interest income ratio, loan loss provision ratio and operation cost efficiency have taken as independent variables. The results of panel data regression analysis showed that credit risk indicator variables of Loan loss provision (LLP), Capital adequacy ratio (CAR), credit interest income (CIR) and size of the bank (SIZE) had positive and statistically significant effect on financial performance of private commercial banks in Ethiopia. And credit risk indicator of Nonperforming loans (NPLs), Leverage ratio (LR) and operational cost efficiency (OCE) had negative and statistically significant effect on banks’ financial performance. Finally, study suggests that Ethiopian commercial banks should/need to work more to improve their financial performance and to reduce their credit risk

| [36] | Mulugeta, W. (2016). The Impact of Credit Risk Management on Performance of Banks. The Case Study of Selected Commercial Banks in Ethiopia (Doctoral dissertation). |

[36]

.

Mekasha also study impact of credit risk management on selected private commercial banks financial performance in Ethiopia. Quantitative data was gathered from secondary data sources which are financial data for the years of 2013 up to 2019 from annual reports of the stated eight selected private banks, it was analyzed and processed through CAMEL approach and ROE to test the existence of the relationship between the selected CAMEL factor measurements with the performance measures for the case of interpretation. A linear regression model was applied to examine the impact of independent variables on the dependent variable for one performance measures. Regression outputs were obtained by using STATA. The regression results revealed that, Capital adequacy ratio and management efficiency ratio has negative significant relationship with ROE but Asset quality ratio has positive significant relationship with ROE and liquidity ratio and earnings ratio has negative in significant relationship with ROE at 95% confidence interval and at 5% level of significance. On the basis of these findings, the study recommends that all CAMEL variables are the key driver of profitability of private banks in Ethiopia similarly the study also identified capital adequacy, management efficiency, earning ability and therefore, Bank managers are advised to give due attention to those variables and to use other mechanisms to improve profitability

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

[34]

.

Consequently, Mengistu, conducted study the Effect of Credit Risk Management on the Profitability Performance of Commercial Bank of Ethiopia proxied by ROA and ROE. The collected data was analyzed by using Time Series data regression model and EView7 software to regress the data, the result showed that credit risk management which is measured by non- performing loan to total loan ratio, and management efficiency that is measured by the ratio of operating expense to total income have negative and significant effect on both dependent variables (ROA and ROE). The other independent variables (CAR, TLTA, NII&LR) are insignificat. The study recommended that the bank’s credit risk management needs strong attention & follow up regarding performer capacetiy building and to review their credit policey & procedure in order to minimize the high incidence of NPL. This is because it has a significant & negative effect on the profitability of the bank, and also Management efficiency result shows that there is a lack of efficiency in expense management since banks pass part of the increased cost to customers and the remaining part to profits. Therefore, the CBE should also give more attention in the reduction of expenses to improve the profitability of the industry

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

[37]

.

Biruk, attempts to reveal the relationship between credit risk and the financial performance of commercial banks in Ethiopia. Panel data from six selected commercial banks covering the ten-year period (2007-2016) is analyzed within the fixed effects model on regression analysis and using E-view8 software. The study used one dependent variable return on asset (ROA), four independent variables that are: nonperforming loan to total loan and advance ratio (NPLTLA), loan provision to total loan and advance ratio (LPTLA), total loan and advance to total deposit ratio (TLATD) and the ratio of non-performing loan to loan provision (NPLLP) as measures of credit risk. Both descriptive statistics and regression analysis specifically fixed effects model were used to analyze the relationships of the depended variable with explanatory variables. The regression result show that non-performing loan to total loan and advance ratio, loan provision to total loan and advance ratio and the ratio of non-performing loan to loan provision show negative and significant effect at 1% and 5% significance level on financial performance of commercial banks in Ethiopia. However, total loan and advance to total deposit ratio show positive and significant effect at 1% significance level on the financial performance of commercial banks in Ethiopia. The research concluded that credit risk has significant effect on the financial performance of commercial banks in Ethiopia

| [11] | Biruk, D. (2015). Assessment of credit risk management practice of commercial bank of Ethiopia (Doctoral dissertation, St. Mary's University). |

[11]

.

Tadesse also conducted his study on the same area. The study used an explanatory research design and the research philosophy adopted was positivism. The target population was 44 commercial banks in Kenya and a census approach was used. Both primary and secondary data were used. Primary data was collected through structured questionnaires and related to credit management practices while secondary data was obtained from review of existing bank loan records in relation to loan amount advanced and non-performing loans for a period of four years from 2015-2018. The data collected was analyzed using both descriptive and inferential statistics with the help of SPSS version 22. The study found out that debt collection policy and lending policy had a positive significant effect on loan performance of commercial banks in Kenya. However, client appraisal had no significant effect on loan performance of commercial banks in Kenya. Therefore, the study concluded that commercial banks’ loan performance could be largely attributed to the efficiency of the credit management practices put in place at the institutions

| [57] | Tadesse, E. (2014). Impact of credit risk on the performance of commercial banks in Ethiopia (Doctoral dissertation, St. Mary's University). |

[57]

.

Finally, Aschis, also study on the effect of credit risk management on profitability of commercial banks of Ethiopia over the period of 2008-2018 G. C. The study employed quantitative research approach with explanatory research design. The secondary data source was employed. The result of regression analysis was applied to investigate the effect of explanatory variables on the profitability. The findings of this study show that, capital adequacy, loan to deposit ratio and loan provision ratio have positive and statistically significant effect on profitability of selected commercial banks in Ethiopia. In opposite direction, non-performing loan, loan to total asset ratio and cost per loan have negative and statistically significant effect on profitability. The profitability measured through ROA was best explained by explanatory variables incorporated in the model. Hence, the researcher suggested that the profitability of commercial banks can be improved through improving credit risk management function of banks by giving attention on the studied variables with statistically significant effect on profitability

| [3] | Aschis, G. (2016). The Impact Of Credit Risk On Financial Performance Of Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

[3]

.

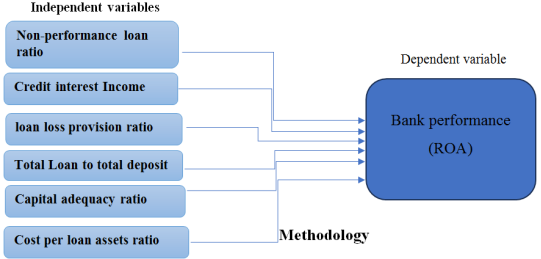

2.5. Conceptual Framework

The conceptual schema of the relationship between the dependent variable (ROA of Commercial banks in Ethiopia) and independent (non-performing loans ratio, credit interest income, loan loss provision ratio, Loan to deposit ratio, Capital adequacy ratio, loan to asset ratio and cost per loan assets ratio) variables are depicted here below.

Figure 1. Conceptual framework of the study Source.

3. Methodology

An explanatory research design was utilized to study the cause-and-effect relationship between independent and dependent variables

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

[34]

. By considering the research problem and objectives, in this study, the quantitative method was used. Quantitative research examines the relationship between variables to evaluate objective theories

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

[37]

. Deductive (quantitative) method as optimal for discovering elements that influence an outcome, the value of an intervention, or knowing the best predictors of outcomes; it is also the greatest approach for testing a theory or explanation

| [15] | Duffie, D., & Singleton, K. J. (2012). Credit risk: pricing, measurement, and management. Princeton university press. |

[15]

. Finally, a mixed methods approach is one in which researchers focus on the study problem and employ all accessible approaches to comprehend it

| [18] | Elgari, M. A. (2003). Credit risk in Islamic banking and finance. Islamic Economic Studies, 10(2). |

[18]

. The study takes seventeen commercial banks (both private and public) as the sample frame to drawing sample size to research. The frame for drawing sample is the level of commercial banks profit (depending on the ranks of banks on their profit) in Ethiopia by taking 13 years data from 2011 to as of June 30, 2023. Thirteen commercial banks was selected for the study include; Commercial bank of Ethiopia (CBE) Awash Bank S. C (AWB), Dashen Bank S. C (DB), Bank of Abyssinia S. C (BOA), Wegagen Bank S. C (WB), United Bank S. C (UB), Nib International Bank S. C (NIB), Cooperative Bank of Oromia (CBO), Lion International Bank (LIB), Oromia International Bank (OIB), Bunna International Bank (BIB), Zemen international bank (ZIB) and Berhan International Bank (BrIB). The rationality for selection was due to availability of structured data and importance of their experience in the industry to understand effect of credit risk on financial performance of Ethiopian commercial bank. The data used for this study is secondary in a nature which was obtained from annual financial reports of commercial banks and publications of the National Bank of Ethiopia (NBE) for bank-specific characteristics and Ministry of Finance and Economic Development (MoFED) for macroeconomic factors. From 2011 to 2023, the data spanned 13 years. To fulfil the study's objective, the researcher used balanced panel data from 2011 to 2023 that gathered through structured document review. The Eviews 12 software was used to conduct descriptive and inferential statistical analysis.

Model Specification

The paper was used the following liquidity management variables: Non-performance loan ratio, interest risk ratio, loan loss provision ratio, total Loan to total deposit ratio (LDR), Capital adequacy (CAP), Liquid assets to total assets ratio (LATAR), and liquid asset to total asset ratio, outcome on financial performance of commercial bank. To examine the effect of explanatory variables on profitability of banks multiple regression models was employed. To represent some omitted variables measurement error and sampling error of the empirical model the study included disturbance (error) term, which represent other variables which was not explained by the independent variables included in the mode.

Based on the above explanation, the models are formulated as follows:

ROA=f(NPLP, ITRR, LLPR, LDR, CAR, LTAR, CLAR)

In connection to above description, the general model for this study, as is found in the existing literature is represented by;

The subscript ‘t’ demonstrates the time-series measurement. The left-hand variable Yt represents the dependent variable in the model, which is the bank’s performance. Xt contains the set of independent variables in the estimation model, is taken to be constant over time t. If α will take to be the same across units, then OLS provides a consistent and efficient estimate of α and β. In the light of the above model, the Panel data was constructed by taking the commercial bank of liquidity risk management using the following multivariate regression model.

ROAit=β0+β1(NPLPit)+β2(ITRRit)+β3(LLPRit)+β4(LDRit)+β5(LTARit)+β6(CLARit)+β + εit,

Where,

ROAit= represents the return on total assets of the selected banks on year t.

NPLR= represents the non-performance loan ratio ith bank on the year t.

CIRit= represents the of credit Interest income ratio ith bank on the year t.

LLPR = represents the Loan loss provision ratio i th bank on the year t.

LDRit= represents the loan-to-deposit ratio of i th bank on the year t.

CAPit= represents the capital adequacy ratio of ith bank on the year t.

LTARit= represents a loan to total asset ratio of ith bank on the year t.

CLARit= represent the cost per loan ratio of i th bank on the year t.

Εit = represents the random error term.

4. Results and Discussion

4.1. Correlation Analysis

Table 1. Presents the correlation coefficients for all the variables considered in this study.

Correlation | ROA | NPL | LTAR | LLPR | LDR | OCER | CIR | CAR |

ROA | 1.000000 | | | | | | | |

NPL | -0.275718 | 1.000000 | | | | | | |

LTAR | 0.026752 | -0.034050 | 1.000000 | | | | | |

LLPR | 0.204170 | 0.256121 | -0.026362 | 1.000000 | | | | |

LDR | 0.593953 | -0.089764 | -0.094360 | 0.106142 | 1.000000 | | | |

OCER | -0.452316 | 0.432326 | 0.038520 | -0.125076 | -0.242300 | 1.000000 | | |

CIR | 0.858490 | -0.148033 | -0.046071 | 0.332933 | 0.459825 | -0.494885 | 1.000000 | |

CAR | 0.130529 | 0.042014 | -0.078768 | 0.195633 | 0.203924 | -0.252473 | 0.147650 | 1.000000 |

Table 1. correlation matrix demonstrates that the loan to asset ratio, capital reserve ratio, total loan to total deposit ratio, credit interest income, and operation cost efficiency ratio (loan loss provision ratio) with respective values of 0.858490, 0.204170, 0.593953, 0.130529, and 0.026752 have positive correlations with the return on asset (dependent variable). However, it had a negative correlation (values of -0.275718, -0.452316, and non-performing loan ratio, respectively) with the cost per loan asset ratio product. Credit interest income out of all the independent variables, have a strong positive correlation with return on asset.

Loan to deposit ratio, and operation cost efficiency ratio out of all the independent variables, have a moderate positive and negative correlation respectively with return on asset. Furthermore, the result also shows that credit interest income, loan loss provision ratio, capital reserve ratio and loan to asset ratio, are slight and small correlated to return on asset. Concluding the analysis, the selected explanatory variables are found to significant relationship with the dependent variable.

4.2. Test of Heteroskedasticity

The condition of classic linear regression model implies that there should be homoscedasticity between variables. This means that the variance should be constant and same. Variance of residuals should be constant otherwise, the condition for existence of regression, homoscedasticity, would be violated and the data would be heteroskedasticity.

To check this, white test applied. Hence, following the general null hypothesis of white, the researcher develops the following hypothesis to check the presence of heteroskedasticity. The findings of the study's white tests to check for heteroskedasticity issues are displayed below.

The following formulation of the heteroskedasticity test's hypothesis was used:

1. H0: There is no Heteroskedasticity problem in the model.

2. H1: There is Heteroskedasticity problem in the model.

Decision Rule: Reject H0 if p-value less than significance level. Otherwise, do not reject H0.

Table 2. White Test of Heteroskedasticity.

Heteroskedasticity Test: White | |

F-statistic | 1.046285 | Prob. F (34, 134) | 0.4126 |

Obs*R-squared | 35.45333 | Prob. Chi-Square(34) | 0.3996 |

Scaled explained SS | 35.94983 | Prob. Chi-Square(34) | 0.3773 |

As it can be seen from

table 2 above, both F-static and Chi-Square versions of the test statistic gave the same conclusion that there is no evidence for the presence of heteroskedasticity, since the p-values of 0.4126 and 0.3996 respectively were in excess of 0.05, so the null hypothesis not rejected. So, this implies that there is no significant evidence for the presence of heteroskedasticity in this research model.

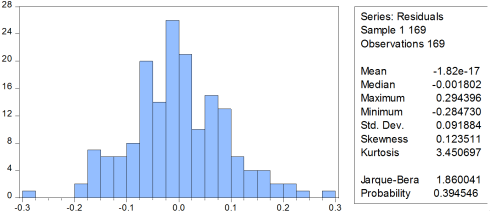

4.3. Normality Test

The normality test was used to assess if a data collection is well-modeled by a normal distribution and to ascertain the probability that an underlying random variable has a normal distribution. The histogram should be bell-shaped and the Jarque-Bera statistic should not be significant if the residuals are regularly distributed. To support the null hypothesis that a normal distribution exists at the 5% level, the p-value shown at the bottom of the normality test screen needs to be greater than 0.05. Jarque-Bera formalizes this by examining the residuals for normality and determining if the coefficients of skewness and kurtosis are around zero and three, respectively.

A measure of a distribution's asymmetry with respect to its mean value is called skewness. Kurtosis is a phrase that implies the "peakness" of the distribution. Three is the kurtosis value of a normal distribution. The Jarque-Bera test for normality is based on two measures that indicate how fat the distribution's tails are: skewness and kurtosis. Even at a 10% significance threshold, it is not anticipated that the Jarque-Bera probability statistics/P-value will be significant. The wording of the null hypothesis for the normality test was as follows:

1. H0: the data is normally distributed.

2. H1: the data is not normally distributed.

If the P-value is less than a significant level, reject H0. Otherwise, H0 should not be rejected.

Figure 2. Histogram Normality test (BJ test).

The histogram depicted in

Figure 2 above has a kurtosis near 3 (or 3.450697) and a skewness that is almost zero (or 0.122411). At the 5% level of significance, the Jarque-Bera statistics (i. e., 0.394546) were not significant, based on the P-values in the histogram. The null hypothesis, which states that the residuals have a normal distribution, therefore does not pass the 5% significance level. Consequently, the error term seems to follow the normal distribution under all conditions, suggesting that conclusions regarding population parameters derived from samples are typically accurate.

4.4. Interpretation of Regression Results

This section goes into great detail on the analysis of the results for each explanatory variable and how important they are in determining the profitability of private banks in Ethiopia. The statistical findings of the study are also compared and contrasted with previous empirical data in the debate. In the sessions that follow, the interpretation of the random effects model regression results and the relationship between the explanatory factors and profitability are thus discussed.

Table 3. Regression result.

Dependent Variable: ROA | | |

Method: Panel EGLS (Cross-section random effects) |

Date: 04/16/24 Time: 14: 22 | | |

Sample: 2011 2023 | | |

Periods included: 13 | | |

Cross-sections included: 13 | | |

Total panel (balanced) observations: 169 | |

Swamy and Arora estimator of component variances |

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

NPL | -0.244656 | 0.058442 | -4.186283 | 0.0000 |

LTAR | 0.099410 | 0.039542 | 2.514053 | 0.0129 |

LLPR | -0.028149 | 0.039821 | -0.706905 | 0.4806 |

LDR | 0.210684 | 0.029639 | 7.108338 | 0.0000 |

OCER | 0.091299 | 0.154162 | 0.592228 | 0.5545 |

CIR | 0.785222 | 0.041653 | 18.85171 | 0.0000 |

CAR | -0.375630 | 0.287586 | -1.306150 | 0.1934 |

C | 0.234745 | 0.027086 | 8.666770 | 0.0000 |

| Effects Specification | | |

| | | S. D. | Rho |

Cross-section random | 0.031901 | 0.4494 |

Idiosyncratic random | 0.035310 | 0.5506 |

| Weighted Statistics | | |

R-squared | 0.875904 | Mean dependent var | 0.148793 |

Adjusted R-squared | 0.870509 | S. D. dependent var | 0.097702 |

S. E. of regression | 0.035158 | Sum squared resid | 0.199009 |

F-statistic | 162.3407 | Durbin-Watson stat | 1.609027 |

Prob (F-statistic) | 0.000000 | | | |

| Unweighted Statistics | | |

R-squared | 0.809683 | Mean dependent var | 0.507011 |

Sum squared resid | 0.334539 | Durbin-Watson stat | 0.957168 |

Empirical model: As presented in chapter three, the empirical model used in the study in order to determine the relationship between independent variable and banks’ return on asset were provided as follows:

ROA =-0.244656*NPL+0.099410*LTAR -0.028149*LLPR +0.210684*LDR+0.091299*OCER -0.785222*CIR-0.375630CAR+ µ

The examination of the findings for each explanatory variable and their impact on the performance of Ethiopian commercial banks is covered in detail in this part. Additionally, the study's statistical results were analyzed in the context of earlier empirical data. As a result, the interpretation of the Random effects model regression results is presented in the following sections. P-value indicates at what percentage or precession level of each variable is significant. R-squared number expresses how well the regression model accounts for the real fluctuations in the dependent variable.

The model's R-squared and adjusted R-squared results were 87% and 87.5%, respectively. The dependent variable, return on asset (ROA) of Ethiopian commercial banks, is well described by the independent factors given in the model, as indicated by the adjusted R-squared value of 87%. As a result, taken as a whole, these factors provide a fair explanation for how credit risks affect Ethiopia's commercial banks' financial performance. Moreover, the F-statistic of 162.3407 and the probability of not rejecting the null hypothesis, which states that there is no statistically significant relationship between the independent variables and the dependent variable, are both 0.000000. These values suggest that the independent variables are all jointly significant in causing variation in the total return on asset, and that the overall model is highly significant at 1%. The panel random effect estimation regression result in the above

table 3 shows that, coefficient intercept (α) is 0.102262. This means, when all explanatory variables took a value of zero, the average value LOA would be take 0.234745 unit and statistically significant at 5% level of significance.

The coefficient for NPL is the only dependant variable that is inversely strong statistically significant impact on return on asset (p-value = 0.0000) at 1% significance level. which indicates that the non-performing loan to loan provision of the commercial banks had negative relationship with ROA and also the relationship is significant at 5% level of significant. However, loan loss provision ration (LLPR) and capital adequacy ratio (CAR) had negative and insignificant impact on return on asset with a p-value of 0.4806 and 0.1934 respectively. The negative relationships indicate that there is an inverse relationship between the explanatory variables and ROA. On the other hand, loan to total asset ratio, loan to deposit ratio and credit interest income ratio have positive effect and significantly affect the value of bank performance. Furthermore, loan to total asset ratio, loan to deposit ratio and credit interest income ratio had a positively and statistically significance impact on return on asset at 1% significance level and at 5% significance level with a p- value of 0.0129, 0.0000, and 0.0000 respectively. Whereas, cost per loan ratio, which is one of independent variables, had a positive and strong statistically insignificant relationship with return on asset with a p-value of 0.5545, which makes it the only variable that has positive and insignificant impact on return on asset.

Hypothesis Testing and Discussion of Results

(i). Non-performing Loan Ratio (NPL) to Return on Asset (ROA)

The coefficient of nonperforming loan ratio (NPLs), which was calculated by dividing nonperforming loans and advances by all loans and advances, is -0.244656 with a p-value of 0.0000, as shown in

table 3. This suggests that the return on asset (ROA) of the sampled private commercial banks would drop by 0.24 percent and be statistically significant at the 1% level of significance when the nonperforming loan ratio (NPLs) increased by one percent, holding other independent variables constant at their average value.

As a result, the null hypothesis that the ratio of non-performing loans has a negative impact on return on asset was not successfully rejected by the researcher. This indicates that the negative correlation between the total amount of loans and advances and nonperforming loans is not well supported by data. The outcome is consistent with other research by

| [3] | Aschis, G. (2016). The Impact Of Credit Risk On Financial Performance Of Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [35] | Million, G., Matewos, K., & Sujata, S. (2015). The impact of credit risk on profitability performance of commercial banks in Ethiopia. African Journal of Business Management, 9, 59-66. |

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [52] | Suganya, S., & Kengatharan, L. (2018). Impact of bank internal factors on profitability of commercial banks in Sri Lanka: a panel data analysis. |

[3, 35, 37, 52]

. which found that NPLs had a detrimental effect on the expansion of financial performance (ROA). The reason for this inverse relationship between nonperforming loans and return on asset could be that when the quantity of nonperforming loans rises, the interest income that the banks receive from these loans falls, which in turn lowers the return on asset. But the result of the study is opposing with the findings of

| [36] | Mulugeta, W. (2016). The Impact of Credit Risk Management on Performance of Banks. The Case Study of Selected Commercial Banks in Ethiopia (Doctoral dissertation). |

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

| [11] | Biruk, D. (2015). Assessment of credit risk management practice of commercial bank of Ethiopia (Doctoral dissertation, St. Mary's University). |

| [17] | Ferreti, F. (2017). Consumer credit information systems: a critical review of the literature. Too little attention paid by lawyers? European Journal of Law and Economics. |

| [26] | Hempel, G., Coleman, A. & Simon, D. (1986), Bank management text and cases, Fourth Edition, John Wiley & Son (Asia) Pte Ltd, New York, 150-175. |

| [56] | Tamrat, W. (2015). Credit Risk Management And Its Impact On Financial Performance Of Ethiopian Private Commercial Banks (Doctoral dissertation, ASTU). |

[36, 34, 11, 17, 26, 56]

which stated that having direct relationship with profitability of commercial banks in Ethiopia.

(ii). Loan to Total Asset Ratio (LTAR) to Return on Asset (ROA)

The result of the random effect model

table 3 indicates that capital structure as measured by total debt to asset had positive relationship with profitability, and statistically significant (p value = 0.0129) at 5% level, which implies that the effect of liquidity on credit risk is statistically significant at α=0.01. This implies that the more banks hold liquid assets, the more will be credit risk. This could be justified on the basis of the logic that credit risk will be higher if firms fail to optimally use the funds for productive purpose. This is because; liquid assets are relatively less productive than loans. debt financing has a positive impact on profitability of Ethiopian banking industry. As a result, the null hypothesis which states there is no significant relationship between liquidity ratio and profitability of core business operations of commercial banks in Ethiopia was rejected. This implies that every change 9 percent (increase or decrease) in banks leverage ratio keeping the other thing constant has a resultant change of percent on the profitability in the same direction. The outcome is consistent with other research

| [36] | Mulugeta, W. (2016). The Impact of Credit Risk Management on Performance of Banks. The Case Study of Selected Commercial Banks in Ethiopia (Doctoral dissertation). |

[36]

, which found that loan to total asset ratio (liquidity ratio) positive relationship with profitability of commercial bank in Ethiopia. However, the result of the study is opposing with the findings of

| [3] | Aschis, G. (2016). The Impact Of Credit Risk On Financial Performance Of Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

[3, 34]

which stated that loan to total asset ratio (liquidity ratio) having negative relationship with profitability of commercial bank in Ethiopia.

(iii). Loan Loss Provision Ratio (LLP) to Return on Asset (ROA)

The ratio of provision for dubious loans to total loan and advances was used to calculate the coefficient of loan loss provision ratio (LLP), which is -0.02814 with a p-value of 0.4806, as

Table 3 above showed. This suggests that when the loan loss provision ratio (LLP) of the sampled private commercial banks increased by one percent, the return on asset (ROA) would decrease by 0.02 percent and become statistically insignificant at the five percent significance level, assuming that all other independent variables remained constant at their average value. The null hypothesis, which states that loan loss provision hurts return on asset, is thus rejected by the researcher. Banks would likely increase their loan loss provisions to offset risk when they invest in riskier assets and lack the skills to manage their lending operations

| [33] | Margaritis, T. (2010). Evaluation of Credit risk based on financial performance, Europian journal of operational research. |

[33]

. Since lending makes up the majority of a bank's business, credit risk is a problem that they must deal with.

To reduce this risk, they establish loan loss provisions. Because the provisions are removed annually from the bank's profits, it has a negative impact on its profitability because a high provision amount limits the bank's ability to provide loans, which lowers profitability. The study is consistent with those of

| [36] | Mulugeta, W. (2016). The Impact of Credit Risk Management on Performance of Banks. The Case Study of Selected Commercial Banks in Ethiopia (Doctoral dissertation). |

| [35] | Million, G., Matewos, K., & Sujata, S. (2015). The impact of credit risk on profitability performance of commercial banks in Ethiopia. African Journal of Business Management, 9, 59-66. |

| [18] | Elgari, M. A. (2003). Credit risk in Islamic banking and finance. Islamic Economic Studies, 10(2). |

| [55] | Teka, B. (2019). Assessment of Credit Risk Management In The Case Of Commercial Bank Of Ethiopia (Doctoral Dissertation, St. Mary's University). |

[36, 35, 18, 55]

who finding that LLP and ROA have a negative association. The study's findings, however, conflict with those of

| [11] | Biruk, D. (2015). Assessment of credit risk management practice of commercial bank of Ethiopia (Doctoral dissertation, St. Mary's University). |

[11]

, who found a direct correlation between loan loss provisions and return on asset.

(iv). Total Loan to Total Deposit Ratio (LDR) to Return on Asset (ROA)

According to the regression analysis, one credit risk dimension total loan and advance to total deposit has a positive correlation (coefficient estimate of 0.210684) with the profitability of Ethiopian commercial banks. The working hypothesis that the ratio of total loan and advance to total deposit has a positive and statistically significant impact on Ethiopian commercial banks' performance was validated by the results, which showed that the relationship is statistically significant at the 1% level of significance (p value = 0.0000). This indicates that the return on asset (ROA) of Ethiopian commercial banks increases by 21% when total loan and advance to total deposit increase by 1% while maintaining other independent variables constant. This result so aligns with the findings of an earlier study by

| [57] | Tadesse, E. (2014). Impact of credit risk on the performance of commercial banks in Ethiopia (Doctoral dissertation, St. Mary's University). |

[57]

, which found that the performance of Ethiopian commercial banks is positively correlated with the total loan and advance to total deposit. Also, some studies found a positive relationship between total loan to deposit and the profitability of commercial banks in Ethiopia

| [33] | Margaritis, T. (2010). Evaluation of Credit risk based on financial performance, Europian journal of operational research. |

| [11] | Biruk, D. (2015). Assessment of credit risk management practice of commercial bank of Ethiopia (Doctoral dissertation, St. Mary's University). |

| [38] | Miranda, M. (2018). Pengaruh Risiko Kredit, Risiko Likuiditas dan Risiko Tingkat Bunga terhadap Return On Asset (ROA): Studi pada PT. Bank Rakyat Indonesia (Persero) Tbk. |

| [49] | Roslan, M., & Rauf, M. (2019). Determinants of profitability of commercial bank a case study of CIMB Bank in Malaysia / Muhammad Rauf Mohd Roslan. |

[33, 11, 38, 49]

. However, thus, this outcome is inconsistent with prior study of

| [1] | Abdirahman, A. (2015). Impact Of Credit Risk Management on Financial Performance of Ethiopian Microfinance Institutions: The Case Study Of Somali Microfinance Institution Share Company (Doctoral dissertation, ASTU). |

[1]

concluded that there is a negative relationship between total loan and advance to total deposit and performance of commercial banks in Ethiopia.

(v). Capital Adequacy Ratio (CAR) to Return on Asset (ROA)

The E-views result of

Table 3 showed that capital adequacy ratio has a negatively and statistically significant with a p – value of 0.1934 and coefficient of -0.375630 Significant effect on banks return on asset, which depicted that holding all the other variables constant, an increase in capital adequacy ratio by one unit leads to increased bank profitability by 37 percent. Based on the findings, the study rejects hypothesis number four namely capital adequacy ratio has a positive effect on banks’ profitability. The outcome confirms the previously held belief that the bigger the bank capital, show the higher the bank profitability. The result of this study is in support of the study of

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [57] | Tadesse, E. (2014). Impact of credit risk on the performance of commercial banks in Ethiopia (Doctoral dissertation, St. Mary's University). |

| [11] | Biruk, D. (2015). Assessment of credit risk management practice of commercial bank of Ethiopia (Doctoral dissertation, St. Mary's University). |

[37, 57, 11]

who found that the rate of capital adequacy ratio has a positive effect on financial performance of private commercial banks and advance. However, contrary to

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [32] | Lee, K., Su, W., & Liu, C. (2017). Operating Performance Evaluation Based on Z-score Model and Profitability between Cross-Straits Credit Cooperatives. Review of Economics and Finance, 10, 72-82. |

[37, 32]

discovered a negative impact of bank capital on bank financial performance. The key claim put forth by these academics supporting the positive correlation between bank capitalization and financial performance is that banks should be better able to offer riskier, longer-term loans if they have a larger capital cushion. Consequently, raising a bank's equity increases its ability to lend more, which raises its revenue and improves its financial performance.

(vi). Credit Interest Income Ratio (CIR) to Return on Asset (ROA)

Table 3 presented that, the coefficient of credit interest income ratio measured by credit interest income to total credit is 0.785222 and its P-value is 0.0000. Holding other independent variables constant at their average value, when credit interest income ratio increased by one percent, return on asset (ROA) of sampled private commercial banks would be increased by 78 percent and statistically significant at 1% level of significant. This indicates that when the interest income from credit activity of the banks increases their income will be high. Therefore, the researcher failed to reject the null hypothesis that credit interest income has positive impact on return on asset. This means, there is no sufficient evidence to support the negative relationship between credit interest income and return on asset. The result of the study is in line with the finding of

| [2] | Ahmadyan, A. (2018). Measuring credit risk management and its impact on bank performance in Iran. Marketing and Branding Research, 5, 168-183. |

[2]

which stated that credit interest income ratio affect return on asset positively and significantly. However, the study is inconsistence with the finding of

| [54] | Shmendi, A. (2019). The Impact Of Credit Risk Management On Financial Performance Commercial Banks Of Ethiopia (Doctoral dissertation). |

[54]

which stated that credit interest income ratio affect return on asset negatively and significantly.

(vii). Operational Cost Efficiency (OCE) to Return on Asset (ROA)

Table 3 indicated that operational cost efficiency has a negative and statistically significant effect on banks performance. Consequently, model result shows the coefficient of the operational cost efficiency which measured by Total amount debit/ total amount of asset is -0.091299 and its p-value is 0.5545. It implies that holding other independent variables constant at their average value, when cash reserve requirement increased by one percent, total loans and advances of sampled commercial banks would be decreased by 9 percent and statistically insignificant at 5% level of significant. Based on the findings, the study reject hypothesis operational cost efficiency has a negative and statistically significant effect on banks performance. The findings are consistent with those of

| [2] | Ahmadyan, A. (2018). Measuring credit risk management and its impact on bank performance in Iran. Marketing and Branding Research, 5, 168-183. |

[2]

, who discovered that operational cost efficiency has a positive and statistically insignificant effect on banks performance.

Some studies

have founda negative and statistically significant association between cost per loan assets and bank profitability

| [34] | Mekasha, G. (2011). Credit risk management and its impact on performance on Ethiopian commercial Banks. Unpublished thesis (Msc), Addis Abeba University. |

| [37] | Mengistu, M. (2018). The Effect Of Credit Risk Management On Profitability Of Selected Commercial Banks In Ethiopia (Doctoral dissertation, St. Mary's University). |

| [57] | Tadesse, E. (2014). Impact of credit risk on the performance of commercial banks in Ethiopia (Doctoral dissertation, St. Mary's University). |

[34, 37, 57]

; this is in not line with researcher expectation. This negative and statistically significant impact of operational cost efficiency on return on asset of private commercial banks in Ethiopia result as bank shift to reduce their costs in order to increase their financial performance. Cos per loans asset is the average cost per loan advanced to the customer in monetary terms, Purpose of this is to indicate efficiency in distributing loans to customers.