The study aims to examine the level of Corporate Environmental Reporting (CER) in relation to corporate characteristics and to identify differences in CER across industry sectors on the Colombo Stock Exchange (CSE). Despite many previous studies on CER practices in developed countries, there is a knowledge gap in less developed countries with low CER status. The study uses descriptive analysis and the Random-Effect Model (REM) for data analysis and hypothesis testing, based on annual reports from 143 listed companies on the CSE from 2017 to 2021. The findings reveal that Sri Lanka has an average level of CER, with the highest level in the Consumer Goods Sector and the lowest in Possession Processing Services. Further, the study identifies that firm size, the use of global standards, and industry sector are determinants of CER, whereas multinational ownership, profitability, and leverage are not associated with CER. The paper has implications for practitioners and policymakers for improving sustainability reporting in developing countries by identifying characteristics that drive CER. This paper is one of the few attempts to use a significantly larger sample to analyse differences in CER in various sectors of CSE.

| Published in | Journal of Finance and Accounting (Volume 14, Issue 2) |

| DOI | 10.11648/j.jfa.20261402.14 |

| Page(s) | 115-138 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Corporate Environmental Reporting, Global Reporting Initiative Guidelines, Listed Companies, Sri Lanka, Corporate Characteristics

Sri Lanka | World | Asia Pacific | India | Pakistan | |

|---|---|---|---|---|---|

Sustainability Reporting Level of Companies | 66% | 80% | 84% | 98% | 90% |

GICS Classification | No. of companies | Stage 1: Strata | Stage 2: Strata | Sample Units |

|---|---|---|---|---|

Automobiles & Components | 1 | Goods | Industrial Goods (IGS) | 34 |

Capital Goods | 29 | |||

Materials | 21 | |||

Utilities | 8 | |||

Consumer Durables & Apparel | 13 | Consumer Goods (CGS) | 45 | |

Household & Personal Products | 2 | |||

Retailing | 14 | |||

Food & Staples Retailing | 3 | |||

Food, Beverage & Tobacco | 47 | |||

Consumer Services | 36 | Services | People Processing (PEPS) | 25 |

Health Care Equipment & Services | 8 | |||

Transportation | 3 | Possession Processing (POPS) | 19 | |

Commercial & Professional Services | 7 | |||

Real Estate | 20 | |||

Energy | 2 | |||

Software & Services | 1 | Information Processing (IPS) | 42 | |

Telecommunication Services | 2 | |||

Banks | 12 | |||

Diversified Financials | 47 | |||

Insurance | 12 | |||

Population size | 288 | Initial Sample Size | 165 | |

Global Reporting Initiatives Standards | ||

|---|---|---|

Code | Description | |

Materials | ||

1 | 301-1 | Total weight or volume of materials that are used to produce and package the organization’s primary products and services |

2 | 301-2 | Percentage of recycled input materials used to manufacture the organization’s primary products and services |

3 | 301-3 | Percentage of reclaimed products and their packaging materials |

Energy | ||

4 | 302-1 | Total energy consumption within the organisation |

5 | 302-2 | Energy consumption outside of the organisation |

6 | 302-3 | The energy intensity ratio for the organisation |

7 | 302-4 | Reduction of energy consumption |

8 | 302-5 | Reductions in energy requirements of products and services |

Water | ||

9 | 303-1 | Water withdrawal by source |

10 | 303-2 | Water sources are significantly affected by the withdrawal of water |

11 | 303-3 | Water recycled and reused |

Biodiversity | ||

12 | 304-1 | Operational sites owned, leased, managed in, or adjacent to, protected areas and areas of high biodiversity value outside protected areas |

13 | 304-2 | Significant impacts of activities, products and services on biodiversity |

14 | 304-3 | Habitats protected or restored |

15 | 304-4 | IUCN Red List species and National Conservation List species with habitats in areas affected by operations |

Emission | ||

16 | 305-1 | Direct (Scope 1) GHG emissions |

17 | 305-2 | Energy indirect (Scope 2) GHG emissions |

18 | 305-3 | Other indirect (Scope 3) GHG emissions |

19 | 305-4 | GHG emissions intensity |

20 | 305-5 | Reduction of GHG emissions |

21 | 305-6 | Emissions of ozone-depleting substances (ODS) |

22 | 305-7 | Nitrogen oxides (Knox), sulfur oxides (SOx), and other significant air emissions |

Effluent and Waste | ||

23 | 306-1 | Water discharge by quality and destination |

24 | 306-2 | Waste by type and disposal method |

25 | 306-3 | Significant spills |

26 | 306-4 | Transport of hazardous waste |

27 | 306-5 | Water bodies affected by water discharges and/or runoff |

Compliance | ||

28 | 307-1 | Significant fines and non-monetary sanctions for non-compliance with environmental laws and/or regulations in terms of: |

Supplier Environmental Assessment | ||

29 | 308-1 | New suppliers that were screened using environmental criteria |

30 | 308-2 | Negative environmental impacts in the supply chain and actions taken |

Variable Type | Variable | Proxy variable | Reference | Definition | Measurement |

|---|---|---|---|---|---|

Dependent variable | CER | CER Index using GRI guideline (CER_index) | [10 , 20, 70, 99, 101] | The proportion of disclosed items for a firm in the given period | 1 when an environment-related item is disclosed and 0 otherwise |

Independent Variables | Firm Size | Ln Total Assets (Ln_TA) | [4 , 7, 47, 70, 72, 101] | Is the sum of both current and non-current assets in the annual report | Natural Log of Total Asset Value (LKR) |

Multinational Ownership | MNC | [40 , 46] | Dichotomous procedure: 1 for if a company is a subsidiary of a Multinational operating in Sri Lanka firms 0 otherwise | 0 = No 1= Yes | |

Profitability | ROE | [4 , 7, 100, 102] | How well does the firm generate returns to its equity providers = PAT / total equity) | Ratio | |

Liquidity | Current ratio (CR) | [ 12, 43, 48, 71, 108] | Measure the firm’s ability to pay its current liability using its current assets. =current assets/ current liabilities | Ratio | |

Usage of CER standards | GRI_usage | [ 40, 87] | Dichotomous procedure: 1 for firms that use GRI guidelines in annual reports and 0 otherwise | 0 = No 1= Yes | |

Industry Type | High Profile Industries Vs Low Profile Industries | [22 , 86, 102] | Dichotomous procedure: 1 for High Profile Industries (IGS, CGS). “0” for Low Profile Industries (PEPS, POPS, IPS) | 0 = PEPS, POPS, IPS 1= IGS, CGS |

CER_INDEX | LN_TA | MNC | ROE | CR | GRI_USAGE | SECTOR | |

|---|---|---|---|---|---|---|---|

Mean | 0.162132 | 22.2102 | 0.09790 | 0.08214 | 4.38593 | 0.272090 | 0.46993 |

Median | 0.066667 | 22.2793 | 0.00000 | 0.06163 | 1.26783 | 0.000000 | 0.00000 |

Maximum | 1.000000 | 27.2784 | 1.00000 | 4.28350 | 253.193 | 1.000000 | 1.00000 |

Minimum | 0.000000 | 12.4930 | 0.00000 | -2.1391 | 0.00313 | 0.000000 | 0.00000 |

Std. Dev. | 0.219514 | 1.7305 | 0.29739 | 0.37951 | 14.36797 | 0.445348 | 0.499444 |

Observations | 715 | 715 | 715 | 715 | 715 | 715 | 715 |

CER_INDEX | LN_TA | MNC | ROE | CR | GRI_USAGE | SECTOR | |

|---|---|---|---|---|---|---|---|

CER_INDEX | 1 | ||||||

LN_MC | 0.463** | 1 | |||||

MNC | -0.02 | -0.082 | 1 | ||||

ROE | 0.237** | 0.211** | 0.036 | 1 | |||

CR | -0.222** | -0.259** | -0.036 | 0.124** | 1 | ||

GRI_USAGE | 0.711** | 0.382** | -0.116** | 0.200** | -0.200** | 1 | |

SECTOR | 0.038 | -0.139** | -0.074 | 0.096** | -0.015 | -0.045 | 1 |

**Significant at 0.001 Level | |||||||

Coefficient | Std. Error | t-Statistic | Prob. | |

|---|---|---|---|---|

LN_TA | 0.0175250 | 0.0035389 | 4.952114 | 0.00000 |

MNC | 0.0367203 | 0.01881245 | 1.951913 | 0.05134 |

ROE | -0.0102637 | 0.0145636 | -0.70475 | 0.48120 |

CR | -0.0001701 | 0.00039078 | -0.43537 | 0.66342 |

GRI_USAGE | 0.3375264 | 0.01353295 | 24.94108 | 0.00000 |

SECTOR | 0.0444038 | 0.01135799 | 3.909474 | 0.00010 |

C | -0.3418088 | 0.07915893 | -4.31801 | 0.00002 |

R-squared | 0.5557465 | Durbin-Watson stat | 0.30483374 | |

Null hypothesis: Residuals are homoscedastic | |||

|---|---|---|---|

Value | df | Probability | |

Likelihood ratio | 1416.876 | 143 | 0.0000 |

Dependent Variable: CER_Index | ||||

|---|---|---|---|---|

Variable | Coefficient | Std. Error | t-Statistic | Prob. |

LN_TA | 0.0137677 | 0.00517649 | 2.659658349 | 0.0080** |

MNC | 0.0167258 | 0.03816675 | 0.438230439 | 0.6613 |

ROE | 0.0020251 | 0.00749592 | 0.270157486 | 0.7871 |

CR | -0.00031 | 0.00029639 | -1.04603075 | 0.2959 |

GRI_USAGE | 0.2475261 | 0.01153344 | 21.46159864 | 0.0000** |

SECTOR | 0.0371292 | 0.02186625 | 1.698012328 | 0.0899* |

C | -0.2289501 | 0.11749093 | -1.94866155 | 0.0517 |

R-squared | 0.9118428 | |||

*Significant at 0.05 and **Significant at 0.01 | ||||

Null hypothesis: REM is appropriate | |||

|---|---|---|---|

Test Summary | Chi-Sq. Statistic | Chi-Sq. d.f. | Prob. |

Cross-section random | 27.92041 | 5 | 0.0547 |

*Significant at 0.05 | |||

CER | Corporate Environmental Reporting |

CSE | Colombo Stock Exchange |

REM | Random-Effect Model |

GRI | Global Reporting Initiative |

ESG | Environmental, Social and Governance |

ROE | Return of Equity |

ROA | Return on Assets |

GICS | Global Industry Classification Standards |

CGS | Consumer Goods Sector |

IGS | Industrial Goods Sector |

PEPS | People Processing Services |

POPS | Possession Processing Services |

IPS | Information Processing Services |

POLS | Pooled Leased Squares Model |

FEM | Fixed-Effects Model |

Ln_TA | Natural Logarithm of Total Assets |

MNC | Multinational Ownership |

CR | Current Ratio |

ICASLL | Institute of Chartered Accountants of Sri Lanka |

PRI | Principles for Responsible Investment |

| [1] | Abdul-Rashid, S. H., Sakundarini, N., Ghazilla, R. A. R., & Thurasamy, R. (2017). The impact of sustainable manufacturing practices on sustainability performance: Empirical evidence from Malaysia. International Journal of Operations & Production Management, 37(2), 182-204. |

| [2] | Adams, C. A., & Larrinaga‐González, C. (2007). Engaging with organisations in pursuit of improved sustainability accounting and performance. Accounting, Auditing & Accountability Journal, 20(3), 333-355. |

| [3] | Ahmad, Z., Hassan, S., & Mohammad, J. (2003). Determinants of Environmental Reporting in Malaysia. International Journal of Business Studies, 11(1). |

| [4] | Aggarwal, P., & Singh, A. K. (2019). CSR and sustainability reporting practices in India: an in-depth content analysis of top-listed companies. Social Responsibility Journal, 15(8), 1033-1053. |

| [5] | Agung, I. G. (2014). Panel Data Analysis Using EViews (1 ed.). Sussex: 4 John Wiley & Sons, Ltd. |

| [6] | Aksan, I., & Gantyowati, E. (2020). Disclosure on sustainability reports, foreign board, foreign ownership, Indonesia sustainability reporting awards and firm value. Journal of Accounting and Strategic Finance, 3(1), 33-51. |

| [7] | Akhter, F., Hossain, M. R., Elrehail, H., Rehman, S. U., & Almansour, B. (2023). Environmental disclosures and corporate attributes, from the lens of legitimacy theory: a longitudinal analysis on a developing country. European Journal of Management and Business Economics, 32(3), 342-369. |

| [8] | Alvesson, M., & Spicer, A. (2019). Neo-Institutional Theory and Organization Studies: A Mid-Life Crisis? Organization Studies, 40(2), 199-218. |

| [9] | An, Y. (2015). Does foreign ownership increase financial reporting quality? Asian Academy of Management Journal, 20(2), 81. |

| [10] | Aruppola, A., & Perera, P. (2013). Environmental Reporting Practice of Listed Companies in Sri Lanka: Evidence from Manufacturing, Motor, Power and Energy Sectors. International Conference on Business and Information. International Conference on Business and Information: University of Kelaniya. |

| [11] | Asrori, A., Amal, M. I., & Harjanto, A. p. (2019). Company Characteristics on the Reporting Index of Corporate Social and Environmental Disclosure in Indonesian Public Companies. International Journal of Energy Economics and Policy, 9(5), 481-488. |

| [12] | Atrill, P., & McLaney, E. (2017). Accounting and Finance: For Non-Specialists (10 ed.). Harlow: Pearson. |

| [13] | Azim, M., Ahmed, E., & D'Netto, B. (2011). Corporate Social Disclosure in Bangladesh: A study of the Financial Sector. International Review of Business Research Papers, 7(2), 37-55. |

| [14] | Baek, H., Kim, B., & Rhee, M. (2014). Effect of Marketing Activities on Financial Performance: An Empirical Analysis. Journal of Marketing Thought, 1(2), 69-79. |

| [15] | Bansal, P. (2005). Evolving sustainably: A longitudinal study of corporate sustainable development. Strategic Management Journal, 26(3), 197-218. |

| [16] | Baltagi, B. H. (2005). Econometric Analysis of Panel Data (3 ed.). Sussex: John Wiley & Sons Ltd. |

| [17] | Bandoi, A., Bocean, C., Del Baldo, M., Mandache, L., M˘anescu, L., & Sitnikov, C. (2021). Including Sustainable Reporting Practices in Corporate Management Reports: Assessing the Impact of Transparency on Economic Performance. Sustainability, 13(940). |

| [18] | Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of management, 17(1), 99-120. |

| [19] | Beddewela, E., & Herzig, C. (2013). Corporate Social Reporting by MNCs' Subsidiaries in Sri Lanka. Accounting Forum, 135-149. |

| [20] | Bhattacharyya, A. (2014). Factors Associated with the Social and Environmental Reporting of Australian Companies. Australasian Accounting, Business and Finance Journal, 8(1), 25-50. |

| [21] | Braam, G. J., Weerd, L. U., Hauck, M., & Huijbregts, M. A. (2016). Determinants of corporate environmental reporting: the importance of environmental performance and assurance. Journal of Cleaner Production, 129, 724e734. |

| [22] | Burgwal, D. V., & Vieira, R. J. (2014). Environmental disclosure determinants in Dutch listed Companies. Revista Contabilidade & Finanças, 25(64), 60-78. |

| [23] | Buysse, K., & Verbeke, A. (2003). Environmental strategy choice and financial profitability: Differences between multinationals and domestic firms in belgium. In Multinationals, Environment and Global Competition (pp. 43-63). Emerald Group Publishing Limited. |

| [24] | Chizema, A., & Buck, T. (2006). Neo-institutional theory and institutional change: Towards empirical tests on the ‘‘Americanization’’ of German executive pay. International Business Review, 15, 488-504. |

| [25] | Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society, 33, 303-327. |

| [26] | Clarkson, P. M., overell, M. B., & Chapple, L. (2011). Environmental Reporting and its Relation to Corporate Environmental Performanceabac_330 27..60. ABACUS, A Journal of Accounting, Finance and Business Studies, 47(1), 27-61. |

| [27] | Colombo Stock Exchange. (2019). Communicating Sustainability Six Recommendations for Listed Companies. Colombo: Colombo Stock Exchange. |

| [28] | Covaleski, M. A., Dirsmith, M. W., & Samuel, S. (1996). Managerial accounting research: the contributions of organizational and sociological theories. Journal of management accounting research, 8. |

| [29] | Cormier, D., Ledoux, M., & Magnan, M. (2011). The Informational Contribution of Social and Environmental Disclosures for Investors. Management Decision, 49(8), 1276 - 1304. |

| [30] | Cowen, S. S., Ferreri, L. B., & Parker, L. D. (1987). The impact of corporate characteristics on social responsibility disclosure: A typology and frequency-based analysis. Accounting, Organizations and Society, 12(2), 111-122. |

| [31] | Cubilla‐Montilla, M. I., Galindo‐Villardón, P., Nieto‐Librero, A. B., Vicente Galindo, M. P., & García‐Sánchez, I. M. (2020). What companies do not disclose about their environmental policy and what institutional pressures may do to respect. Corporate Social Responsibility and Environmental Management, 27(3), 1181-1197. |

| [32] | da Silva Monteiro, S. M., & Aibar‐Guzmán, B. (2010). Determinants of environmental disclosure in the annual reports of large companies operating in Portugal. Corporate Social Responsibility and Environmental Management, 17(4), 185-204. |

| [33] | D’Amico, E., Coluccia, D., Fontana, S., & Solimene, S. (2016). Factors influencing corporate environmental disclosure. Business Strategy and the Environment, 25(3), 178-192. |

| [34] | Darnall, N., Henriques, I., & Sadorsky, P. (2008). Do environmental management systems improve business performance in an international setting? Journal of International Management, 14(4), 364-376. |

| [35] | Daubeney, H. (2021). What is the big news at COP26 for ESG reporting? Retrieved January 1, 2022, from Pwc: |

| [36] | Deegan, C., & Gordon, B. (1996). A study of the environmental disclosure practices of Australian corporations. Accounting and business research, 26(3), 187-199. |

| [37] | De Grosbois, D. (2012). Corporate social responsibility reporting by the global hotel industry: Commitment, initiatives and performance. International Journal of Hospitality Management, 31(3), 896-905. |

| [38] | De Grosbois, D. (2016). Corporate social responsibility reporting in the cruise tourism industry: a performance evaluation using a new institutional theory based model. Journal of Sustainable Tourism, 24(2), 245-269. |

| [39] | DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 147-160. |

| [40] | Dissanayake, D., Tilt, C., & Qian, W. (2019). Factors influencing sustainability reporting by Sri Lankan companies. Pacific Accounting Review, 31(1), 7-92. |

| [41] | Dissanayake, D., Tilt, C., & Xydias-Lobo, M. (2016). Sustainability reporting by publicly listed companies in Sri Lanka. Journal of Cleaner Production, 129, 169-182. |

| [42] | Fabian, O., & Emeka, O. (2022). Effects of Environmental Reporting on Liquidity of Firms in Nigeria. Asian Journal of Advances in Research, 15(2), 36-46. |

| [43] | Fallan, E., & Fallan, L. (2019). Corporate tax behavior and environmental disclosure: Strategic trade-offs across elements of CSR? Scandinavian Journal of Management, 35, 101042. |

| [44] | Freeman, R. E. (1984). Stockholders & Stakeholders: A New Perspective on Corporate Governance. California Management Review, 25, 88-106. |

| [45] | Frost, G. R., & Wilmshurst, T. D. (2000, December). The Adoption of Environment‐related management accounting: an analysis of corporate environmental sensitivity. In Accounting Forum (Vol. 24, No. 4, pp. 344-365). Taylor & Francis. |

| [46] | Gao, S. S., Heravi, S., & Xiao, J. Z. (2005). Determinants of corporate social and environmental reporting in Hong Kong: a research note. Accounting Forum, 29(2), 233-242. |

| [47] | Garba, I., & Mauda, A. B. (2020). Environmental Reporting Practices in Select Listed Companies in Nigeria: A Study. PDUAMT Business Review, 2, 33-44. |

| [48] | Garg, M., & Kumar, S. (2018). he Relationship Between Corporate Environmental Reporting Practices and Company Characteristics: Evidence from India. ournal of Accounting Research & Audit Practices, 17(3). |

| [49] | Gauthier, J. (2013). Institutional theory and corporate sustainability: Determinant versus interactive approaches. Organization Management Journal, 10(2), 86-96. |

| [50] | Gerged, A. (2021). Factors affecting corporate environmental disclosure in emerging markets - the role of corporate governance structures. Business Strategy and the Environment, 30(1), 609-629. |

| [51] | Gioia, D. A., & Pitre, E. (1990). Multiparadigm perspectives on theory building. Academy of Management Review, 15(4), 584-602. |

| [52] | Global Sustainability Standards Board. (2016). Consolidated Set of GRI Sustainability Reporting Standards 2016. Global Sustainability Standards Board. |

| [53] | González‐Benito, J., & González‐Benito, Ó. (2006). A review of determinant factors of environmental proactivity. Business Strategy and the Environment, 15(2), 87-102. |

| [54] | Grant, R. M. (1991). The resource-based theory of competitive advantage: implications for strategy formulation. California management review, 33(3), 114-135. |

| [55] | Gray, R., Bebbihgton, J., & Walters, D. (1993). Accounting for environment. London: Paul Chapman). |

| [56] | GRI. (2022). About GRI. Retrieved January 2, 2022, from |

| [57] | GRI South Asia Network; (2023). Sustainability Reporting In Sri Lanka 2023, Connecting the Dots. |

| [58] | Gujarati, G. N., Porter, D. C., & Gunasekar, S. (2012). Basic Econometrics (5 ed.). McGraw-Hill Education (India) Private Limited. |

| [59] | Guthrie, J., & Abeysekera, I. (2006). Content Analysis of Social, Environmental Reporting: What is New? Journal of Human Resource Costing & Accounting, 10(2), 114-126. |

| [60] | Haladu, A., & Salim, B. B. (2016). Corporate ownership and sustainability reporting: Environmental agencies’ moderating effects. International Journal of Economics and Financial Issues, 6(4), 1784-1790. |

| [61] | Hassan, T. (2010). Corporate Social Responsibility Disclosure: An Examination of Framework of Determinants & Consequences. PhD Thesis. UK: Durham University. |

| [62] | Henri, J.-F., & Journeault, M. (2010). Eco-control: The influence of management control systems on environmental and economic performance. Accounting, Organizations and Society, 35(1), 63-80. |

| [63] | Higgins, C., & Larrinaga, C. (2014). 16 Sustainability reporting. Sustainability Accounting and Accountability, 273. |

| [64] | Ho, L. C., & Taylor, M. E. (2007). An Empirical Analysis of Triple Bottom-Line Reporting and its Determinants: Evidence from the United States and Japan. Journal of International Financial Management and Accounting, 18(2), 123-152. |

| [65] | Hopper, T., & Hoque, Z. (2006). Triangulation approaches to accounting research. Methodological Issues in Accounting Research: Theories and Methods, 477-486. |

| [66] | Hoque, Z., Covaleski, M. A., & Gooneratne, T. N. (2013). Theoretical triangulation and pluralism in research methods in organizational and accounting research. Accounting, Auditing & Accountability Journal, 26(7), 1170-1198. |

| [67] | Hsu, C., Choon Tan, K., Hanim Mohamad Zailani, S., & Jayaraman, V. (2013). Supply chain drivers that foster the development of green initiatives in an emerging economy. International Journal of Operations & Production Management, 33(6), 656-688. |

| [68] | Humphrey, C., & Scapens, R. W. (1996). Methodological themes: theories and case studies of organizational accounting practices: limitation or liberation? Accounting, Auditing & Accountability Journal, 9(4), 86-106. |

| [69] | Iarossi, J., Miller, J. K., O’Connor, J., & Keil, M. (2011). Addressing the sustainability challenge: Insights from institutional theory and organizational learning. First International Conference on Engaged Management Scholarship. |

| [70] | Ika, S. R., Rahayu1, R., Elrif, M. Y., & Widagdo, A. K. (2021). Environmental reporting, ownership structure and corporate characteristics of Indonesian listed companies. IOP Conf. Series: Earth and Environmental Science, 724. |

| [71] | Islam, J., Roy, S. K., Miah, M., & Das, S. K. (2020). A Review on Corporate Environmental Reporting (CER): An Emerging Issue in the Corporate World. Canadian Journal of Business and Information Studies, 2(3), 45-53. |

| [72] | Jariya, A. M. (2015). Environmental Disclosures in Annual Reports of Sri Lankan Corporate: A Content Analysis. Journal of Emerging Trends in Economics and Management Sciences, 6(8), 350-357. |

| [73] | Jennings, P. D., & Zandbergen, P. A. (1995). Ecologically sustainable organizations: An institutional approach. Academy of Management Review, 20(4), 1015-1052. |

| [74] | Jessop, A., Wilson, N., Bardecki, M., & Searcy, C. (2019). Corporate Environmental Disclosure in India: An Analysis of Multinational and Domestic Agrochemical Corporations. Sustainability, 9(4843), 1-33. |

| [75] | Joudeh, A. H., Almubaideen, H. I., & Alroud, S. F. (2018). Environmental disclosure in the annual reports of the Jordanian mining and extraction companies. Journal of Economics, Finance and Accounting, 5(1), 18-25. |

| [76] | Khalid, T. B. (2015). An Analysis of Disclosure of Social and Environmental Responsibility and Stakeholders Perceptions - The Case of Jordan. Dundee: the Abertay University. |

| [77] | Khan, A., Muttakin, M. B., & Siddiqui, J. (2012). Corporate governance and corporate social responsibility disclosures: evidence from an emerging economy. Journal of Business Ethics, 114(2), 207-223. |

| [78] | Khlif, H., Guidara, A., & Souissi, M. (2015). Corporate social and environmental disclosure and corporate performance Evidence from South Africa and Morocco. Journal of Accounting in Emerging Economies, 5(1), 51-69. |

| [79] | Kılıç, M., Uyar, A., Kuzey, C., & Karaman, A. S. (2021). Does institutional theory explain integrated reporting adoption of Fortune 500 companies? Journal of Applied Accounting Research, 22(1), 114-137. |

| [80] | Kinn, S., & Curzio, J. (2005). Integrating qualitative and quantitative research methods. Journal of Research in Nursing, 10(3), 317-336. |

| [81] | KPMG. (2020). The KPMG Survey of Sustainability Reporting 2020. KPMG. |

| [82] | Krueger KPMG. (2020). The KPMG Survey of Sustainability Reporting 2020. KPMG. |

| [83] | Krueger, P., Sautner, Z., Tang, D. Y., & Zhong, R. (2024). The effects of mandatory ESG disclosure around the world. Journal of Accounting Research, 62(5), 1795-1847. |

| [84] | Kumar, K., & Prakash, A. (2019). Examination of sustainability reporting practices in Indian banking sector. Asian Journal of Sustainability and Social Responsibility, 4(2), 1-36. |

| [85] | Kuzey, C., & Uyar, A. (2017). Determinants of sustainability reporting and its impact on firm value: Evidence from the emerging market of Turkey. Journal of Cleaner Production, 143, 27-39. |

| [86] | Laguir, I., Stagliano, R., & Elbaz, J. (2015). Does corporate social responsibility affect corporate tax aggressiveness? Journal of Cleaner Production, 107, 662-675. |

| [87] | Looser, S., & Wehrmeyer, W. (2016). Ethics of the firm, for the firm or in the firm? Purpose of extrinsic and intrinsic CSR in Switzerland. Social Responsibility Journal, 12(3), 545-570. |

| [88] |

Lounsbury, M., & Zhao, E. Y. (2020). Neo-institutional Theory. Retrieved January 5, 2022, from

https://www.oxfordbibliographies.com/view/document/obo-9780199846740/obo-9780199846740-0053.xml |

| [89] | Lozanoab, R., Nummertc, B., & Ceulemansd, K. (2016). Elucidating the relationship between Sustainability Reporting and Organisational Change Management for Sustainability. Journal of Cleaner Production, 125, 168-188. |

| [90] | Maas, K., & Rosendaal, S. (2016). Sustainability targets in executive remuneration: Targets, time frame, country and sector specification. Business Strategy and the Environment, 25(6), 390-401. |

| [91] | Masud, M. A., Bae, S. M., & Kim, J. D. (2017). Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh. Sustainability, 9(1717), 1-19. |

| [92] | Ministry of Environment. (2011). National Green Reporting System of Sri Lanka - Reporting Guidelines. Ministry of Environment. |

| [93] | Ministry of the Environment. (2004). Environmental Reporting Guidelines. Tokiyo: Ministry of the Environment, Japan). |

| [94] | Modell, S. (2015). Theoretical triangulation and pluralism in accounting research: a critical realist critique. Accounting, Auditing & Accountability Journal, 28(7), 1138-1150. |

| [95] | Mohamed Adnan, S., van Staden, C., & Hay, D. (2014). The Legitimacy of Institutional Theory: The Case of CSR Reporting in Cross-Cultural Settings. Chris and Hay, David, The Legitimacy of Institutional Theory: The Case of CSR Reporting in Cross-Cultural Settings (September 18, 2014). |

| [96] | Mokhtar, N., Jusoh, R., & Zulkifli, N. (2016). Corporate characteristics and environmental management accounting (EMA) implementation: evidence from Malaysian public listed companies (PLCs). Journal of Cleaner Production, 136, 111-122. |

| [97] | Mudiyanselage, N. C. (2018). Corporate Govvernance. Board involvement in corporate sustainability reporting: evidence from Sri Lanka, 6(1042-1056), 18. |

| [98] | Nimanthi, D. K., & Priyadarshanie, W. A. (2021). Environmental Disclosure Practice and Firm Performance: Evidence from Sri Lanka. International Journal of Accounting & Business Finance, 7(2), 75-91. |

| [99] | Niresh, J. A., & Silva, W. H. (2018). The extent of corporate social responsibility disclosure practices: evidence from the banks, finance and insurance sector in Sri Lanka. Global Journal of Management and Business Research, 17(2), 2249-4588. |

| [100] | Nuskiya, M. N., Ekanayake, A., Beddewela,,. E., & Gerged, A. M. (2021). Determinants of corporate environmental disclosures in Sri Lanka: the role of corporate governance. Journal of Accounting in Emerging Economies, 11(3), 367-394. |

| [101] | Nwobu, O. A., & Ngwakwe, C. C. (2020). Corporate Responsibility Reporting in Africa: The Effect of Macroeconomic Indicators and Political Regime. Asian Economic and Financial Review, 10(10), 1203-1219. |

| [102] | Ortiz, M. G., & Grado, C. P. (2016). Information on corporate social responsibility and institutional theory. Intangible Capital, 12(4), 942-977. |

| [103] | Oliver, C. (1991). Strategic responses to institutional processes. Academy of Management Review, 16(1), 145-179. |

| [104] | Otley, D. (1999). Performance management: a framework for management control systems research. Management accounting research, 10(4), 363-382. |

| [105] | Pedrini, M., & Ferri, L. M. (2019). Stakeholder management: a systematic literature review. Corporate Governance: The International Journal of Business in Society, 19(1), 44-59. |

| [106] | Philips, C. (2016). Effect of environmental disclosures on liquidity of listed manufacturing firms in France. European Journal of Business and Management, 2(1), 14-23. |

| [107] | Powell, D. (2016). Quantile regression with nonadditive fixed effects. Quantile Treatment Effe, 1-28. |

| [108] | Preuss, L. (2012). Responsibility in Paradise? The Adoption of CSR Tools by Companies Domiciled in Tax Havens. Journal of Business Ethics, 110, 1-14. |

| [109] | Qu, W., Leung, P., & Cooper, B. (2013). A Study of Voluntary Disclosure of Listed Chinese Firms A Stakeholder Perspective. Managerial Auditing Journal, 28(3), 261-294. |

| [110] | Raar, J. (2002). Environmental Initiatives: Towards Triple-bottom Line Reporting. Corporate Communications: An International Journal, 7(3), 169-183. |

| [111] | Rugman, A. M., & Verbeke, A. (1998). Corporate strategies and environmental regulations: An organizing framework. Strategic management journal, 19(4), 363-375. |

| [112] | Rafique, M. A., Malik, Q. A., Waheed, A., & Khan, N. U. (2017). Corporate Governance and Environmental Reporting in Pakistan. Pakistan Administrative Review, 1(2), 103-114. |

| [113] | Rajapakse, B. (2003). Environmental Reporting Practices of the Private Sector Business Organizations in Sri Lanka. Journal of Management, 1(1), 11-21. |

| [114] | Rajeshwaran, N., & Ranjan, R. P. (2013). An Investigation of Voluntary Environmental Reporting Practices of Sri Lankan Listed Companies. Colombo: Annual Research Sessions, Faculty of Graduate Studies, University of Colombo. |

| [115] | Ramadhan, B. Y., & Nuswantara, D. A. (2019). Corporate Social Responsibility Regulation and Tax Aggressiveness (SOEs Case). ” in International Conference on Economics, Education, Business and Accounting, KnE Social Sciences, 927-937. |

| [116] | Sahay, A. (2004). Environmental Reporting by Indian Corporations. Corporate Social Responsibility and Environmental Management, 11, 1-13. |

| [117] | Sarivudeen, A., & Sheham, A. (2013). Corporate governance practices and environmental reporting: a study of selected listed companies in Sri Lanka. International Research Conference on Innovative Perspective in Business, Finance and Information Managment (pp. 284-291.). South Eastern University of Sri Lanka. |

| [118] | Saunders, M., Lewis, P., & Thornhill, A. (2016). Research Methods for Business Students (7 ed.). Harlow: Pearson. |

| [119] |

Schiopoiu, B. A., & Popa, I. (2013). Legitimacy Theory. Retrieved January 2, 2022, from Encyclopedia of Corporate Social Responsibility. Springer:

https://link.springer.com/referenceworkentry/10.1007%2F978-3-642-28036-8_471#howtocite |

| [120] | Shamil, M. M., Shaikh, J. M., Ho, P. L., & Krishnan, A. (2014). The influence of board characteristics on sustainability reporting Empirical evidence from Sri Lankan firms. Asian Review of Accounting, 22(2), 78-97. |

| [121] | SheConsults (Pvt) Ltd. (2015). Sustainability Reporting in Sri Lanka: The Big Picture. |

| [122] | Smith, M., Yahya, K., & Amiruddin, M. (2007). Environmental Disclosure and Performance Management. Asian Review of Accounting, 15(2), 185-199. |

| [123] | Smith, J., Haniffa, R., & Fairbrass, J. (2011). A conceptual framework for investigating ‘capture’in corporate sustainability reporting assurance. Journal of Business Ethics, 99, 425-439. |

| [124] | Solikhah, B. (2016). An overview of legitimacy theory on the influence of company size and industry sensitivity towards CSR disclosure. International Journal of Applied Business and Economic Research (IJABER), 14(5), 3013-3023. |

| [125] | Stakeholder Theory. (2018). About. Retrieved January 2, 2022, from |

| [126] | The World Bank. (2021). Economic and Poverty Impact of COVID-19. The World Bank. |

| [127] | Tregidga, H., Milne, M., & &Kearins, K. (2009). Organisational Legitimacy and Social and Environmental Reporting Research: The Potential of Disclosure Analysis. Accounting, Auditing and Accountability Journal, 1-19. |

| [128] |

Ullah, M. H., Yakub, K. M., & Hossain, M. M. (2013). Environmental Reporting Practices in Annual Report of Selected Listed Companies in Bangladesh. Research Journal of Finance and Accounting

www.iiste.org 4(7), 45-60. |

| [129] | Wagner, R., & Seele, P. (2017). Uncommitted deliberation? Discussing regulatory gaps by comparing GRI 3.1 to GRI 4.0 in a political CSR perspective. Journal of Business Ethics, 146, 333-351. |

| [130] | Wang, M. C. (2017). The Relationship between Firm Characteristics and the Disclosure of Sustainability Reporting. Sustainability, 9(624), 114. |

| [131] | Wangombe, D. K. (2013). Multi-Theoretical Perspective of Corporate Environmental Reporting: A Literature Review. Society of Interdisciplinary Business Research, 2(2), 655-674. |

| [132] | Wilmshurst, T. D., & Frost, G. R. (2000). Corporate environmental reporting: A test of legitimacy theory. Accounting, Auditing & Accountability Journal, 13(1), 10-26. |

| [133] | Wirtz, J., & Lovelock, C. (2022). Services Marketing: People, Technology, Strategy (9 ed.). Hackensack: World Scientific. |

| [134] | Wooldridge,,. J. (2010). Econometric analysis of cross section and panel data (2 ed.). Massachusetts Institute of Technology. |

| [135] | Yale Center for Environmental Law & Policy. (2022). Environmental Performance Index- Sri Lanka. Retrieved August 8, 2022, from |

| [136] | Ylönen, M., & Laine, M. (2015). For logistical reasons only? A case study of tax planning and corporate social responsibility reporting. Critical Perspectives on Accounting, 33, 5-23. |

APA Style

Edirisinghe, N. D., Edirisinghe, U. C. (2026). Determinants of Corporate Environmental Reporting: Evidence from Sri Lanka. Journal of Finance and Accounting, 14(2), 115-138. https://doi.org/10.11648/j.jfa.20261402.14

ACS Style

Edirisinghe, N. D.; Edirisinghe, U. C. Determinants of Corporate Environmental Reporting: Evidence from Sri Lanka. J. Finance Account. 2026, 14(2), 115-138. doi: 10.11648/j.jfa.20261402.14

@article{10.11648/j.jfa.20261402.14,

author = {Navoda Dhanangika Edirisinghe and Udani Chathurika Edirisinghe},

title = {Determinants of Corporate Environmental Reporting: Evidence from Sri Lanka},

journal = {Journal of Finance and Accounting},

volume = {14},

number = {2},

pages = {115-138},

doi = {10.11648/j.jfa.20261402.14},

url = {https://doi.org/10.11648/j.jfa.20261402.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jfa.20261402.14},

abstract = {The study aims to examine the level of Corporate Environmental Reporting (CER) in relation to corporate characteristics and to identify differences in CER across industry sectors on the Colombo Stock Exchange (CSE). Despite many previous studies on CER practices in developed countries, there is a knowledge gap in less developed countries with low CER status. The study uses descriptive analysis and the Random-Effect Model (REM) for data analysis and hypothesis testing, based on annual reports from 143 listed companies on the CSE from 2017 to 2021. The findings reveal that Sri Lanka has an average level of CER, with the highest level in the Consumer Goods Sector and the lowest in Possession Processing Services. Further, the study identifies that firm size, the use of global standards, and industry sector are determinants of CER, whereas multinational ownership, profitability, and leverage are not associated with CER. The paper has implications for practitioners and policymakers for improving sustainability reporting in developing countries by identifying characteristics that drive CER. This paper is one of the few attempts to use a significantly larger sample to analyse differences in CER in various sectors of CSE.},

year = {2026}

}

TY - JOUR T1 - Determinants of Corporate Environmental Reporting: Evidence from Sri Lanka AU - Navoda Dhanangika Edirisinghe AU - Udani Chathurika Edirisinghe Y1 - 2026/04/14 PY - 2026 N1 - https://doi.org/10.11648/j.jfa.20261402.14 DO - 10.11648/j.jfa.20261402.14 T2 - Journal of Finance and Accounting JF - Journal of Finance and Accounting JO - Journal of Finance and Accounting SP - 115 EP - 138 PB - Science Publishing Group SN - 2330-7323 UR - https://doi.org/10.11648/j.jfa.20261402.14 AB - The study aims to examine the level of Corporate Environmental Reporting (CER) in relation to corporate characteristics and to identify differences in CER across industry sectors on the Colombo Stock Exchange (CSE). Despite many previous studies on CER practices in developed countries, there is a knowledge gap in less developed countries with low CER status. The study uses descriptive analysis and the Random-Effect Model (REM) for data analysis and hypothesis testing, based on annual reports from 143 listed companies on the CSE from 2017 to 2021. The findings reveal that Sri Lanka has an average level of CER, with the highest level in the Consumer Goods Sector and the lowest in Possession Processing Services. Further, the study identifies that firm size, the use of global standards, and industry sector are determinants of CER, whereas multinational ownership, profitability, and leverage are not associated with CER. The paper has implications for practitioners and policymakers for improving sustainability reporting in developing countries by identifying characteristics that drive CER. This paper is one of the few attempts to use a significantly larger sample to analyse differences in CER in various sectors of CSE. VL - 14 IS - 2 ER -

Cardiff School of Management, Cardiff Metropolitan University, Cardiff, United Kingdom

Department of Accountancy and Finance, Sabaragamuwa University of Sri Lanka, Belihuloya, Sri Lanka

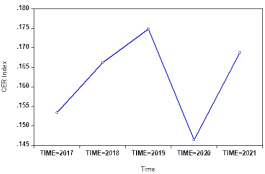

Figure 1. Average Level of CER Overtime.

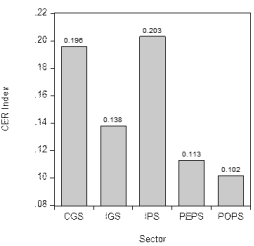

Figure 2. Average Level of CER by Sectors.

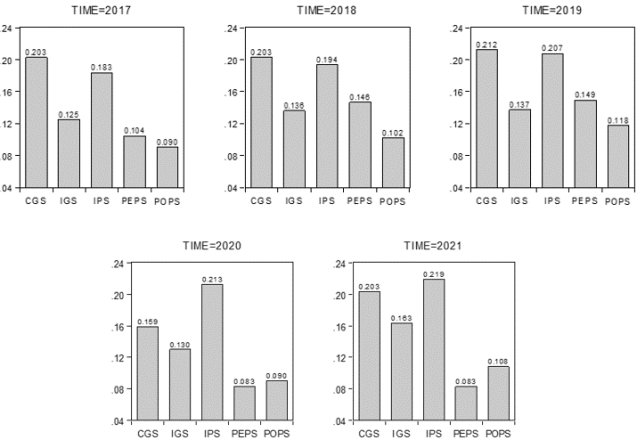

Figure 3. Average Level of CER by Year and Sector.

Figure 4. Average level of CER by GRI usage.

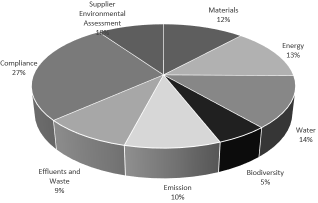

Figure 5. Average CER by Disclosure Theme.

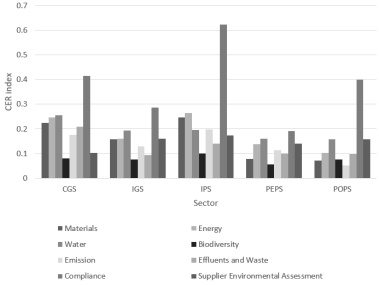

Figure 6. Average CER by Theme by Sector.

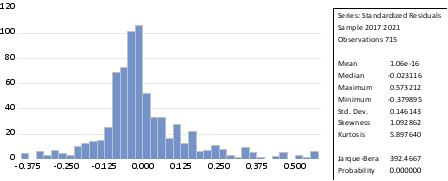

Figure 7. Normality Test for Residuals.